Labor and Employment

OK at Work: How Will the Newest Supreme Court Decision Affect Your Business?

On this week's OK at Work, Sarah Sawyer and Russell Berger discuss the Supreme Court's recent decision eliminating the substantial deference that federal courts previously gave to the decisions of administrative agencies and what it could mean for business owners, executives, and in-house counsel. Listen to learn more.

July 30, 2024

Family Law

My Spouse Had an Affair. What Rights Do I Have?

A question divorce attorneys are frequently asked is, “how will my spouse’s affair impact my divorce?” There are a few things to consider when dealing with adultery in divorce proceedings. Grounds for Divorce. As of October 2023, adultery is no longer grounds for divorce in Maryland. In fact, Maryland has abolished its fault-based grounds for divorce and now only recognizes three no-fault grounds: 6-month separation, irreconcilable differences, and mutual consent. Alimony. A judge will evaluate several factors when considering whether or not to award a party alimony, including the duration and amount. One of the factors is the circumstances leading to the divorce. This is where adultery comes into play. If your spouse had an affair, and financial support is necessary to maintain a reasonable standard of living or to become self-supporting, proving adultery could be an important factor in your alimony case. Property Division. Similar to alimony, property division is a factor-based inquiry where fault, including adultery, is considered. The court will analyze a multitude of factors when determining how to divide marital property, so it is important to address each factor that is relevant to your claim, including your spouse’s affair. Custody. Contrary to what most believe, adultery does not weigh heavily on a court’s decision about custody of minor children. It is often the case that someone can be a poor spouse but a good parent. However, suppose the adulterer is making poor judgment decisions about the children due to their extramarital affair (for example, taking the children to bars or leaving them unattended to spend time with a paramour). In that case, a court may weigh this behavior when determining parental fitness. It is hard enough to face the reality of dissolving a marriage, but finding out your spouse is having an affair will make an already difficult situation almost impossible. The emotional aspect of adultery is one of the biggest hurdles to a successful, amicable divorce. That is why it is important to have an experienced, skilled attorney who can objectively evaluate each fact related to your case to help you achieve a favorable outcome.

July 29, 2024

Franchise Law

Franchise Sales Likely to Get New Level of Regulation Over Third-Party Sellers

A bill passed by the California Senate on May 22, 2024, Senate Bill No. 919 (“Bill 919”), will address a gap in the regulation of franchise sales – namely, a lack of transparency regarding the role and background of independent franchisee recruiters, often known as “franchise brokers.” This bill, which has the rare support of both the International Franchise Association (the “IFA”) and franchisee advocate groups such as the American Association of Franchisees and Dealers (“AAFD”), now heads to the California General Assembly for approval. It appears to have a strong chance to become law this year and to influence franchise sales regulation nationally. Historically, franchise laws have focused on requiring affirmative disclosures by franchisors so that franchisee prospects can obtain information about the franchise system to better understand the business opportunity that they are evaluating. While the vast majority of franchise registration states require franchisors to submit information about their third-party brokers in franchise seller disclosure forms, those provisions pre-dated the growth of franchise seller networks such as FranNet, FranChoice and The Entrepreneur’s Source (among many others). Such intermediary companies, which usually identify themselves as consultants to prospective franchisees, are a major source of new franchisees to many growing systems and play an important role in franchise sales. Because those companies have many franchises in their “inventory” (sometimes hundreds) and therefore only occasional contact with each franchisor, they don’t fit the model of a broker regularly engaged in selling for a relatively small group of brands who the franchisor would recognize as its regularly used franchise seller. To date, only two states (New York and Washington), have historically required brokers to register themselves as franchise sellers. If passed, Bill 919 would require third-party franchise sellers, including the large networks with dozens of individual representatives, to register with the State of California. The fee for a franchise seller filing an initial registration application is $250, with a $150 annual renewal fee and $50 fee to amend a registration upon a material change to the application information. More notably, Bill 919 adds a requirement for third-party franchise sellers to provide a disclosure document to prospective franchise buyers. The broker would be required to disclose some of the categories of information that franchisors must supply in their Franchise Disclosure Document (“FDD”). Specifically, brokers must submit a Uniform Third-Party Franchise Seller Disclosure Form and a Uniform Third-Party Franchise Seller Disclosure Document (“FSDD”) along with their registration application. In addition to registering the FSDD with the state, franchise sellers must also present this document to a prospective franchisee prior to engaging with them about a franchise opportunity. The FSDD must include the following information: A cover page containing standardized and general language that is not specific to a particular broker and will include, at a minimum, the following information: A description of the types of franchise sellers A seller’s role in the sales process The services a seller might provide Methods of compensation for a seller’s services Examples of questions a prospective franchisee might ask a seller General information about the specific seller’s legal and trade names, state and year of formation, principal address, owners and key personnel, and contact information The franchise seller’s professional experience during the last five years Administrative, civil, or criminal actions against the seller within the last five years alleging fraud, unfair or deceptive practices, or similar violations (which aligns with the types of matters disclosed in Item 3 of a franchisor’s FDD) The industries a seller represents and the number of brands within each industry A description of services provided by the seller How the seller is actually compensated, including how the amount of compensation is calculated Whether a broker network/organization or franchise sales organization may receive additional consideration The name and contact information for every franchisee that the seller sold a franchise to anywhere in the United States during the last calendar year, including the number of units sold to each franchisee With respect to enforcement, Bill 919 creates a cause of action that allows franchisees to sue for damages and rescission if the seller violates the law with respect to a franchise sale. Additionally, the California commissioner can issue a stop order prohibiting a franchise seller from offering or selling franchises in the state if it finds that a seller has failed to comply with any applicable provisions of law or rules issued by the commissioner. The new rules and penalties have the same scope as a franchise sale under the California Franchise Investment Laws. So, they will apply to franchise sellers who are based in California, but also to anyone “consulting with” a prospective franchisee who is a resident of or has a principal place of business in California, or if the franchised business will be in California. Any franchise broker that wishes to sell franchises that will be located in California, or to prospects located in California, will need to register. The bill exempts California licensed real estate brokers and securities brokers-dealers. Since none of the mandatory disclosure items are limited to California sellers or California franchisees, Bill 919 also may be a template for the regulation of franchise sellers on a nationwide level, particularly in those other states that require pre-sale registration of franchise offerings. If passed, Bill 919 will go into effect on July 1, 2025.

July 29, 2024

Mergers and Acquisitions

Delaware Passes Amendments to Delaware’s Corporate Law to Override Judicial Precedents and Simplify Corporate Governance in M&A Transactions.

Changes to the Delaware General Corporation Law (“DGCL”) were signed into law last week by Governor John Carney. SB313 will now take effect on August 1, 2024, and will apply retroactively to all agreements (including merger agreements) made by a Delaware corporation and all agreements and instruments approved by the board of directors of a Delaware corporation, except for the agreements and board action in pending litigation on or prior to August 1, 2024. These changes were in response to several Delaware Chancery Court (“Court”) rulings affecting stockholder agreements, merger agreements and corporate governance requirements applicable to merger transactions. The amendments propose a legislative override over recent decisions to implement changes that allow for greater freedom of contract for stockholder and merger agreements and the elimination of technical, seemingly non-material governance requirements applicable to merger transactions. A new DGCL § 122(18) permits corporations to convey the rights to consent and approval of corporate action to persons through stockholder agreements unless such conveyance is specifically prohibited by the corporation’s certificate of incorporation. This amendment nullifies the recent decision in West Palm Beach Firefighters’ Pension Fund v. Moelis & Co. where the Court found a stockholder agreement requiring the majority stockholder’s approval for certain corporate actions “an impermissible internal governance restriction” in violation of DGCL § 141. Addressing the Court’s finding of a violation of DGCL § 251(b) when the board approved a draft version of the merger agreement in Sjunde Ap-Fonden v. Activision Blizzard, Inc., the new DGCL § 147, eliminates the requirement for board approval of the ‘final form’ of agreement if, at the time of approval, all of the material terms are determinable through information and materials presented to or known by the board, and second, the new DGCL § 268(b) clarifies that disclosure schedules and the like are not required to be a part of the merger agreement for board approval pursuant to DGCL § 251(b). Doubling up on the results of Activision, in response to the Court’s finding of a violation of DGCL § 251(c) where the corporation had included a brief summary of the merger agreement in the proxy statement sent with a separate notice to the stockholders that did not include a brief summary of the merger agreement, a new DGCL § 232(g) allows a corporation to satisfy the stockholder notice requirement for a merger agreement when such agreements and brief summaries are “enclosed with the stockholder notice or annexed or appended to the notice.” A third byproduct of the Activision decision, a new DGCL § 268(a) allows a board to approve and file a certificate of incorporation of the surviving corporation of a merger following the effectiveness of the merger if the surviving entity will be wholly-owned and controlled by the buyer and all of the shares of capital stock of the constituent corporation issued and outstanding immediately before the effective time of the merger are converted into or exchanged for cash, property, rights or securities (other than stock of the surviving corporation). In Crispo v. Musk, the Court denied a stockholder plaintiff’s claim for lack of standing where the plaintiff sued for ‘lost stockholder premium’ damages despite a provision in the merger agreement that specified that the buyer would be liable for ‘lost stockholder premium’ in the event buyer breached the merger agreement. DGCL § 261(a)(1) specifically allow parties to a merger agreement to include provisions requiring the payment of penalties and ‘lost stockholder premiums’ in the event the merger is not consummated and allow parties to enforce these payment provisions. New DGCL § 261(a)(2) confirms that the stockholders of a constituent party to a merger agreement may irrevocably appoint one or more persons to serve as a representative of all stockholders and delegate to such person the exclusive authority to enforce the rights of all stockholders under such agreement, after consummation of the transaction as an agent of the stockholders of the constituent corporation whose shares are canceled and converted in the merger into the right to receive cash or other property, and to enter into a binding settlement on behalf of all shareholders, a principal of corporate law. Seemingly, this amendment codifies stockholder representative authority articulated by the Court in Aveta Inc. v. Cavallieri, where the Court found that the stockholders were bound to the results of a post-closing adjustment and subsequent arbitration decision when the stockholders appointed a stockholder representative to represent the stockholders and the representative utilized facts ascertainable outside the merger agreement to derive post-closing adjustments on behalf of all stockholders using a calculation method clearly and expressly set forth in the merger agreement and subsequently pursued the final determination through the use of a neutral arbitrator.

July 25, 2024

Mergers and Acquisitions

Fine Wine, Cheese and M&A?

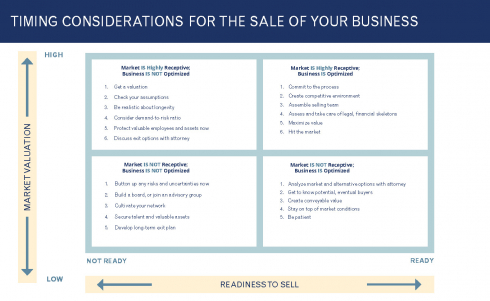

What do wine and cheese have to do with M&A? Well, unlike fine wine and good cheese, M&A transactions don’t age well (I heard this analogy recently at a TAB Board meeting). M&A transactions are driven by timing considerations, both internal and external. Market conditions continually change and having your transaction consummated when the market is most receptive is paramount. Missing the mark can have heavy consequences on items such as taxation or valuation. Likewise, internal commitment and momentum make for efficient transactions. Deals require continual, steady movement forward; transactions without momentum waffle and struggle to gain pace. Some timing can be controlled by the parties. For example, responding to inquiries and questions as quickly as possible. Letting emails sit, even for a day, can have major impacts given that most M&A transactions have many parties involved. Slow-moving parties can trigger rippling impacts that may lead to unintended consequences. M&A transactions do not adhere to a 9 am to 5 pm workday. I always advise clients, especially sell-side clients, that they should work their business 9 am to 5 pm and sell their businesses 5 pm to midnight (and of course weekends). Like a marathon runner, M&A deals need to find the pace and stick to that pace to finish the race strong! Originally posted 1/22/21, no content changes.

July 24, 2024

Environmental and Sustainability

Businesses May Face Challenges in Reauthorization of Wetlands Approvals After NJDEP Decision

Businesses in New Jersey seeking reauthorization of wetlands approvals may now be required to go through the more intensive individual permit process following a unique decision involving a wetlands permit issued to the New Jersey Department of Transportation (NJDOT). While this decision is somewhat unique as it involves a state agency as the permittee, it likely will limit the New Jersey Department of Environmental Protection’s (NJDEP) authority to reauthorize previously approved structures, activities, and features. In the latest development of this ongoing legal saga, In the Matter of Reauthorization of The Freshwater Wetlands General Permit #1 and Permit Modifications, Docket No. A-2758-21 (App. Div. June 7, 2024), the Appellate Division vacated the issuance of a Freshwater Wetlands General Permit by the NJDEP to the NJDOT. This permit was intended for the rehabilitation of a Confined Disposal Facility (CDF) to store dredged materials from multiple waterways. (A CDF is a structure planned and designed to receive sediments dredged from a waterway. Its primary function is to safely contain these materials, preventing contamination from reentering the waterway. In New Jersey, CDFs are critical in environmental management and sediment control.) The Permitting of the CDF and Subsequent Challenges The CDF at issue here was initially authorized in 1983 for the storage of dredged material from a single waterway. In 2018, NJDEP issued several permits to NJDOT in connection with the dredging of three waterways: Westecunk Creek, Parkers Run, and Cedar Run. This included a General Permit #1 authorizing the rehabilitation of the CDF. By way of background, a General Permit #1 allows the repair or replacement of a previously authorized, serviceable structure that lawfully existed before July 1, 1988, in freshwater wetlands. Eligibility for a General Permit #1 requires that: “(1) [t]he previously authorized structure... has not been and will not be put to any use other than as specified in any permit authorizing its original construction” and “(2) [t]he activities do not expand, widen, or deepen the previously authorized feature, and do not deviate from any plans of the original activity,” except for certain “minor deviations.” N.J.A.C. 7:7A-7.1(a). In 2021, based on challenges from local residents and environmental groups, the Appellate Division remanded the issuance of the General Permit to NJDEP for further consideration. After additional review, NJDEP reauthorized the General Permit in 2022. The present appeal arises from further challenges to this 2022 approval by local residents and environmental groups. The Appellate Division’s Rejection of the General Permit In a rare rejection of the deference owed to the NJDEP, the Appellate Division determined that NJDEP could not issue a General Permit #1 for the CDF due to differences between the initially authorized CDF activities and the currently proposed CDF activities under the new permit. Specifically, the Appellate Division found that the original 1983 permit only authorized the CDF to store dredged spoils from Westecunk Creek. In contrast, the General Permit allowed the CDF to store materials from three waterways. Therefore, the General Permit violated the requirement of N.J.A.C. 7:7A-7.1(a)(1), which prohibits “any use other than” what was originally authorized. Additionally, the Appellate Division concluded that the General Permit improperly “expanded” the CDF in violation of N.J.A.C. 7:7A-7.1(a)(2) because it authorized storage of nearly five times the originally permitted material. The Appellate Division also made noteworthy determinations regarding the continuity of the CDF’s operations despite the facility remaining dormant for many years, which could benefit developers and businesses in other contexts. Wetlands Approvals: Implications of Recent Appellate Division and Chevron Decisions As noted above, this unique decision may make it harder for businesses and developers to obtain reauthorization of wetlands approvals without pursuing an individual permit. When pursuing any development or rehabilitation projects, it is critical to consult with experienced professionals and legal counsel to develop a permitting strategy. As a final matter, this decision was rendered before the United States Supreme Court overturned the long-established Chevron deference, which also limited an agency’s ability to interpret its own regulations. As a result, while it was not informed by the reversal of Chevron deference, the Appellate Divisions rejection of the determination of NJDEP here may be a harbinger of a shift in treatment of NJDEP decisions by the New Jersey courts.

July 24, 2024

Intellectual Property

Protecting Your Most Important Asset: Why Trademark Registration Matters

What would you do with an asset with an almost infinite lifespan that symbolizes your company to your customers? And if that asset was your company’s most valuable asset? You’d protect it, of course. If you run a business of any type, you have such an asset: a trademark, often referred to as a brand name. The question is, are you protecting it? Trademarks reportedly account for about one-third of the stock market value of companies in the S&P 500. If your company is not protecting one of its most important assets, it is putting that asset at risk. The first step in protecting a trademark is registering it with the U.S. Trademark Office. This legal process is best handled by lawyers and involves some costs. In many cases, the cost to register in the U.S. is under $5,000, although it can exceed that amount. Renewal costs are generally under $2,500, with renewal needed every ten years. Given the nearly unlimited lifespan of a trademark, these costs are well worth it when considering the benefits of registration. Banks Will Take Trademarks as Collateral for Loans Some banks, such as IDB, will accept a security interest in a company’s trademarks as collateral for a loan. In today’s business landscape, where many businesses operate virtually and lack significant physical assets, having an asset that a bank can lend against can be crucial for a company’s growth. However, without a registered trademark, a bank may be unwilling to lend against it. At best, the bank may impose higher lending costs if it is willing to lend against unregistered trademarks. Parties Doing Business with a Company Want Assurance that the Company’s Brand is Protected Investors considering investing in a company will want to see that it has taken steps to protect its trademarks. As part of their due diligence efforts, they will ask for the details of trademark applications or registrations. If there are no applications or registrations, providing a transparent and honest explanation is necessary. Potential partners, such as licensees or franchisees, will also want to see that the company has taken steps to protect its trademarks if they invest money to do business with the company, whether by opening a franchised store or manufacturing and selling licensed goods; these partners will want assurance that the company has protected their mutual investment. Trademarks are Crucial to a Company’s Value As noted, a significant portion of a company’s value can be attributed to its brand. Companies with strong brands deliver better value to their shareholders.[1] The value of those assets is critical in business valuations, mergers, or acquisitions, providing leverage and opportunities for future sales and expansion. If you are considering selling your business and retiring, trademark registration can significantly increase its value. Given this potential boost, isn’t the cost of registration worth it? Trademark Registrations May Prevent Others from Registering the Same or a Similar Mark Trademark registrations are listed in the Federal Trademark Office’s online database, which is publicly available and searchable. Anyone searching for a similar trademark should find any registrations that your company owns. Upon discovering your company’s registration, third parties may drop or change their plans. Additionally, when the Trademark Office examines applications filed by others, it will refuse the registration of the same or similar marks for the same or related goods and services. However, if your mark is not registered, the Trademark Office will not block the registration of the same or a similar mark. The Trademark Office only reviews its records during the examination process. It does not search the marketplace, which can result in a competitor registering a similar mark. While it is possible to challenge such a registration, doing so can be costly in terms of time and money. It is far better to prevent this situation by ensuring your mark is registered in the first place. While the Trademark Office will block potentially infringing third-party applications, it does not take action to stop third parties from infringing your company’s trademark. The responsibility to enforce trademark rights falls on the trademark owner. Further, once your company’s mark is registered, you gain nationwide rights that can be enforced against subsequent users. Without a registration, your rights are limited to the geographic area in which your company operates. One other thing. Forming a company with the state is not the same as registering a trademark. The state does not check to see if your name will infringe on anyone else’s name when you form a company. Having a Trademark Registration Makes Enforcement Easier on Online Platforms If someone uses your mark without authorization on social media or an online shopping platform, having a trademark registration makes it easier to enforce your company’s rights and have the online platform take action to stop the infringement. A registration allows the platform to verify your rights, which they cannot do if your company has no trademark registration. Additionally, a trademark registration grants your company access to online protection mechanisms, such as Amazon’s Brand Registry. In cybersquatting cases, which still occur, having a trademark registration simplifies proving your case and recovering the domain name in question. However, a trademark registration does not automatically entitle your company to the corresponding domain name. Legal Benefits of Registration Having a trademark registration provides certain legal advantages. For example, lawsuits for infringement of federal trademark registrations can be filed in federal court. In such cases, registration entitles the trademark owner to a legal presumption of ownership, the right to use the mark, and the mark’s validity (validity presumption applies only to registrations on the Principal Register). These presumptions can streamline court proceedings and reduce legal expenses. Without registration, your company must prove ownership, usage rights, and protection eligibility in every enforcement action, resulting in increased costs. Additionally, marks registered on the Principal Register can achieve incontestable status after five years of registration, provided an appropriate filing is made with the Trademark Office. Incontestable status means the registration can only be challenged on specific, limited grounds. Furthermore, registered marks can use the ® symbol to indicate they are registered. This can prevent third parties from adopting similar marks and, more importantly, prevent infringers from arguing in a lawsuit that your company waived its right to damages by not using the ® symbol. Using the ® symbol helps ensure you do not inadvertently leave money on the table. Foreign Trademark Registrations A U.S. trademark registration does not afford trademark protection outside the U.S.; trademark rights must be protected country by country. However, a U.S. trademark registration can serve as the basis for trademark filings abroad and enable your company to benefit from certain international treaties that may reduce the cost of filing in other countries. Recording Registrations with Customs and Border Protection (CBP) A trademark registration on the Principal Register can be recorded with Customs and Border Protection (CBP). However, there is a fee for this service. Recording your registration with CBP allows them to monitor goods coming into the country. If CBP identifies goods with an infringing or counterfeit mark, they will stop their importation and seize the items. While CBP may request verification that the goods are not legitimate, once that confirmation is provided, CBP will manage the seizure process. Conclusion Trademark registration offers several cost-saving benefits. Legal presumptions and the status of incontestable registrations can reduce court costs. Additionally, registered marks make it easier to enforce rights online. A U.S. trademark registration can also reduce the costs of filing for registrations in other countries and can be recorded with CBP to assist in enforcing your rights. Beyond these cost-reducing benefits, trademarks are high-value assets that can serve as collateral for loans and that investors and business partners will want to see. Therefore, trademarks should be protected with the same diligence as any other asset. Failing to protect this asset can result in its loss and a subsequent loss in value for the company — an outcome no company would or should permit. [1] See The top 100 most valuable global brands 2013 (marketingweek.com).

July 24, 2024

Business

Figure These Two Things Out Before You Sell Your Business

Your business is in good shape and you’re feeling ready to sell. You have your key value drivers in place: skilled employees, strong sales numbers, a pattern of consistent growth. You’ve assembled an advisory team, conducted a thorough sweep of your organizational records, and eliminated the proverbial skeletons in your closet. You’ve also performed the deep, difficult work of preparing yourself emotionally and psychologically for the journey ahead. Time to hit the gas—right? Perhaps, not quite yet. Yes, all of the above are fundamental success factors and important steps to take before engaging in a merger, acquisition, or another type of business transaction. But they’re only the basics. Polishing every surface and tightening every screw won’t make a difference if the business isn’t built on a rock-solid foundation. To adequately prepare for M&A, business owners need to proactively strategize and fortify their organizations for potential curveballs. As a seller, you need to think ten steps ahead of a buyer. You need to know what they want before they want it. It pays to err on the side of paranoia. Here are two critical questions every seller must answer before stepping into the market: 1. Is the Business Structured Correctly? One factor sellers frequently ignore is business entity structure. The way your business is structured today may not be the ideal structure during an M&A transaction. Say your company is operating as an S corporation. You have detailed records of your finances and meetings, a strong leadership team in place, and—best of all—lower taxes than you’d have if the company was structured differently. You may think this shows prudent business management—and in most cases, it would. In M&A, however, S corps at times fare poorly. That’s because certain buyers like to acquire LLC interests—not S corporation stock. The same vehicle that may shield you from high tax payments may create obstacles for a buyer during a sale. In an environment less robust than the current market, it even could cause a potential buyer to pass on the deal. Thus, as an S corporation owner, you may need to do an “F-reorganization,” a tax-free structuring technique that changes your business so that you’re selling LLC interests. A corporate restructure may improve your chances of closing the eventual sale. If you do have to restructure, you’ll need to do so in the pre-transaction phase. 2. Are Employees in It for The Long Run? Your people are the lifeblood of your business. Without them, your organization wouldn’t be worth what it is, nor would it be well-equipped for continued success in the future. Most sellers realize this, and yet a fair number neglect to lock down their key employees until well into the transaction. These business owners compartmentalize the deal and their day-to-day business operations separately. What they don’t realize is one domain frequently spills over into the other. A rocky M&A negotiation damages employee morale, and vice versa. By the time a transaction is nearly consummated, an ill-prepared business may have missed projections or dropped in value due to unexpected employee departures. Always stay focused on your employee engagement and retention rates—before and during the transaction. Figure out how you’ll incent your people to cooperate and continue performing at their best while the deal is pending, and to stay with the new ownership after you’ve closed. Put plans into place early, well in advance of courting a buyer. The longer you wait, the less effective your efforts will be. For sellers, employee retention and business structure are two vital pre-transaction considerations. But they’re only a couple of many. If you’re thinking about selling your business, you need to prepare for anything and everything that could go wrong. Familiarize yourself with Murphy’s law, and start strategizing as soon as possible. Forethought and planning today can save you serious time, money, and frustration tomorrow. Originally posted 12/20/2019, no content changes

July 18, 2024

Labor and Employment

California Labor & Employment Update: PAGA Reform

On July 1, 2024, Governor Newsom signed Senate Bill 92 and Assembly Bill 2288, amending The Private Attorneys General Act (PAGA). The amendments are effective June 19, 2024, but do not affect civil actions that were filed or cases where the required notice to the employer and the Labor Workforce Development Agency (“LWDA”) was submitted prior to June 19, 2024. The amendment was a compromise reached among Governor Newsom, business leaders and the unions to remove a measure to repeal PAGA from the November ballot. PAGA has been tough on businesses in California. While the amendments are helpful, businesses still need to be vigilant to avoid the penalties under PAGA. PAGA was enacted in California in 2004, allowing employees to file lawsuits against employers for violations of the labor code on behalf of themselves, other employees, and the state of California. The law essentially deputizes employees to act as private attorneys general and to pursue civil penalties for violations that would typically only be enforceable by state labor agencies. If an employee believes there has been a violation of the California Labor Code by their employer, the employee can then file a claim under PAGA. Claims can include a broad range of violations ranging from overtime to meal and rest breaks. Part of the penalties recovered are distributed to the state, with affected employees and their legal representation receiving the remainder. The following summarizes the most significant changes to PAGA: Individual Plaintiffs Must Have Suffered a Violation for Each Claim Made in their Complaint. There are several changes to PAGA, but the most significant for businesses is that a plaintiff be able to prove that they were subject to the specific PAGA violations upon which their complaint is based. Previously, a plaintiff, with one violation, could allege that the employer violated every section of the Labor Code. For example, if the plaintiff only suffered meal period violations, they cannot now bring an action for unpaid overtime. While this should limit some PAGA litigation and penalties, it will probably result in multi-plaintiff lawsuits, with employee plaintiffs alleging that they suffered differing violations. Ability to Cure Once a Labor and Workforce Development Agency Notice if Received. The amendments expand when employers can cure violations when they receive the LWDA notice to avoid PAGA litigation. However, it is unclear in the new legislation exactly how much is needed to cure the violation and make the employee whole. What this provision does do is make it more important for employees to immediately contact counsel once they receive an LWDA notice to be able to audit their practices and attempt to cure them where allowed. Early evaluation conference. The bill would also authorize an employer who employed at least 100 employees and who has been served with a summons and complaint asserting a claim under PAGA to file a request and participate in an early evaluation conference and to request a stay of court proceedings. The employer has the ability to cure violations by using this procedure. The requirements are very specific and must occur shortly after the service of any action on the employer. As a result, employers should take care to avail themselves of this new procedure because if the employer cures the violations as set forth in the procedures for the Early Evaluation Conference, the penalties are capped at $15 per employee. Penalty Reductions. One of the most difficult elements of PAGA are the penalties. The new legislation: (a) revises the penalty structure and reduces it in certain situations; (b) encourages compliance with labor laws by capping penalties on employers who quickly take steps to fix policies and practices and make workers whole after receiving a PAGA notice, as well as on employers that act responsibly to take steps proactively to comply with the labor code before even receiving a PAGA notice; (c) creates new, higher penalties on employers who act maliciously, fraudulently or oppressively in violating labor laws; and (d) ensures that more of the penalty money goes to employees by increasing the amount allocated to employees from 25% to 35%. Some examples of reduced penalties are as follows: Penalty Cap Reductions for Employers Who Take “All Reasonable Steps” to Comply with the Labor Code. Penalties are reduced by 15% or 30% if a person accused of a violation has taken all reasonable steps to comply with the provisions alleged to have been violated in the required notice provided by the aggrieved employee. Reasonable steps may include, but are not limited to, any of the following: (1) The employer conducted periodic payroll audits and took action in response to the results of the audit. (2) The employer disseminated lawful written policies. (3) The employer trained supervisors on applicable Labor Code and wage order compliance or took appropriate corrective action with regard to supervisors. The amendments to PAGA state that whether the employer’s conduct was reasonable shall be evaluated by the totality of the circumstances and take into consideration the size and resources available to the employer and the nature, severity and duration of the alleged violations. The amendments further provide that the existence of a violation, despite the steps taken, is insufficient to establish that an employer failed to take all reasonable steps. Employers with Weekly Pay Periods. The amendments reduce penalties for employers with weekly pay periods by one-half, effectively calculating penalties as if the employer had bi-weekly pay periods. PAGA has significantly impacted labor law enforcement in the state, and these new reform measures will hopefully streamline the law even further. Employers should work with legal counsel to fully understand the details of this reform and any action that should be taken at this time. Given the new penalty structure, employers need to act quickly once they receive notice of a potential PAGA action. Quick action can help to reduce and/or eliminate some of the penalties.

July 17, 2024

Estates and Trusts

Estate Planning for Young Professional Athletes: A Comprehensive Guide

The Barclay’s Center in Brooklyn recently buzzed with the first round of the NBA draft — a gathering of young, exceptionally talented players hoping to be drafted to a professional team, the pinnacle and the reward for years of hard work and dedication. As young athletes, their focus rightly revolves around training, competition, and achieving a peak performance. However, it's also important for them to consider their financial future, particularly given the short average duration of an athletic career —only 3.5 to 5.6 years, according to The Bleacher Report. As a result, it is imperative that young athletes start off on the right foot immediately to protect their hard-earned assets, their potentially brief career, and their loved ones. While so many assume that the topic of estate planning is for an older demographic, beginning early can provide peace of mind and secure the athlete’s hard-earned wealth for the future. Why Should Young Athletes Consider an Estate Plan? Financial Security: While athletes can earn significant income early in their careers, the average professional athlete only earns between $362,000 - $680,000 per season, according to the Motley Fool. Proper estate planning is key to ensuring that the young athlete’s assets, whether substantial or not, are managed and protected, providing a stable and secure financial future beyond their career. Uncertainty of Career Length: The length of a professional athlete’s career is highly unpredictable. Injuries, even minor ones, can abruptly end a career or lead to being sidelined, benched, traded, or marginalized. Additionally, the physical demands of professional athlete’s training schedules and physical demands can diminish athletic abilities over time. An estate plan serves as a safety net in case of unexpected events. Family Protection: Many athletes come from families that have collectively pooled their resources to provide the support that propelled the young athlete to the professional arena. When athletes succeed, they often want to protect those who have supported them. The athlete is often relied upon to ensure financial security for themselves and their larger family of origin. An estate plan ensures that the athlete and their family are protected, especially if their career ends earlier than expected. The “Plays” of an Athlete’s Estate Plan Last Will and Testament: A Will is a legal document that outlines how assets will be distributed after death. It names beneficiaries, designates guardians for minor children, and appoints an executor to carry out the athlete’s wishes. Trusts: Often referred to as a Will “substitute,” Trusts offer more privacy, control, and flexibility over the athlete’s asset distribution than a Will. Trusts also help minimize estate taxes, protect assets from creditors and other predatory actors, and provide for loved ones in a structured manner. Power of Attorney: This document grants the athlete’s trusted advisor the authority to make financial decisions on the athlete’s behalf, especially during busy times like pre-season training. If the athlete becomes incapacitated, even temporarily, the Power of Attorney allows another trusted person to make financial decisions on their behalf. It's crucial for the athlete to choose someone who understands their unique financial situation and has their best interests at heart. Healthcare Proxy: Similar to a Power of Attorney, a Healthcare Proxy appoints a person to make medical decisions on behalf of the athlete if the athlete is unable to do so themselves. This ensures that the athlete’s healthcare wishes are respected when they are unable to make decisions themselves. Beneficiary Designations: Often overlooked, beneficiary designations on accounts direct who inherits the asset upon the athlete’s death. It is imperative that the athlete review and update beneficiary designations on life insurance policies, retirement accounts from their respective league, and other financial instruments regularly to ensure they align with the athlete’s Will, Trust, and overall estate plan. The Young Athlete’s Next Move: Assess Your Assets: The young athlete should start simple: list all their assets, including property, investments, intellectual property, and personal items. Set Goals: Determine the goals for the estate plan. What is most important? There is no one right answer: every athlete has different priorities, whether it be financial security for the family, a charitable cause, or minimizing taxes. Regardless of the goal, it can be achieved with the right plan. Consult Professionals: Avoid cautionary tales of athletes who engaged unqualified “professionals” (here’s looking at you, Tim Duncan.) Working with an experienced estate planning attorney, a competent financial advisor, and a skilled accountant will ensure a comprehensive estate plan structured and tailored to the young athlete’s needs. Regular Reviews: The life circumstances of young athletes change frequently. Being traded to a team in a new state with different estate planning rules, experiencing drastic income fluctuations, and evolving interpersonal relationships mean the estate plan must pivot to remain relevant. Regular reviews ensure the plan continues to reflect current circumstances. Estate planning can seem daunting, especially for young athletes just starting their careers. However, taking the time to plan now can provide significant benefits in the future. By securing their financial future, protecting their assets, and ensuring their loved ones are cared for, young athletes can focus on what they do best on the field, the court, or the ice.

July 12, 2024

Business

Supreme Court Overturns Chevron Deference in Landmark Loper Bright Decision

On June 28, 2024, the Supreme Court issued its decision in Loper Bright v. Raimondo and Relentless v. Department of Commerce. As expected, following oral argument, the Court overruled the Chevron deference doctrine in a 6–3 decision written by Chief Justice John Roberts. The doctrine stems from a 1984 Supreme Court case, Chevron U.S.A., Inc. v. Natural Resources Defense Council, Inc, 467 U.S. 837 (1984), establishing a two-step analysis for judicial review of statutory interpretation. Under Chevron, if a court concluded that a statute was silent or ambiguous, it had to defer to an agency’s permissible construction of the statute. Now, under Loper Bright, courts must “exercise their independent judgment” and “may not defer to an agency interpretation of the law simply because a statute is ambiguous.” Supreme Court Review: Chevron Doctrine's Applicability to Cases Post-Loper Bright In Loper Bright, two sets of fishing companies challenged a rule issued by the National Marine Fisheries Service requiring vessels operating in the Atlantic herring market to pay for a government-certified observer during their fishing trips. Applying Chevron, the district court in each case rejected the companies’ challenge to the observer rule and granted summary judgment to the government. Panels of the U.S. Courts of Appeals for the D.C. Circuit and First Circuit affirmed these decisions. The U.S. Supreme Court granted certiorari in both cases on the limited question of whether Chevron should be overruled or clarified. Supreme Court's Interpretation of APA in Loper Bright The Loper Bright decision is premised on what the majority believes is a plain text reading of the Administrative Procedure Act (APA), which governs judicial challenges to agency actions. The Court specifically determined that the APA, which was not considered in Chevron, reflects the traditional understanding of the judiciary's role. This role requires courts to independently interpret the meaning of laws. The Court dismissed the notion of a “presumption” of agency expertise, explaining that resolving unclear laws falls within the court’s jurisdiction, not the agencies. Put another way, while courts may use an agency’s interpretation to help “inform their inquiry,” they cannot dictate how courts interpret the law. The Loper Bright Court also rejected the idea that Chevron promotes consistency, highlighting inconsistencies in its application. Furthermore, it concluded that adherence to Chevron is not mandated by stare decisis. Chevron had proven “unworkable” because determining whether a statute is ambiguous is an indeterminate exercise. Consequently, the Court vacated and remanded the lower court’s decisions. Supreme Court Opinion: Chief Justice Roberts and the Majority Chief Justice Roberts delivered the opinion of the Court, in which Justices Thomas, Alito, Gorsuch, Kavanaugh, and Barrett joined. Justices Thomas and Gorsuch each filed concurring opinions. Justice Kagan filed a dissenting opinion, in which Justices Sotomayor and Jackson joined.

July 12, 2024

Family Law

What Happens to the Marital Home During Divorce?

The marital home is often one of the most significant and emotionally charged assets in a divorce. Deciding what happens to the home can be a complex and contentious process involving both financial considerations and personal attachments. There are options with regard to the Marital Home, including: Selling the HomePros: Selling the marital home is a common option, as it allows both parties to liquidate the asset and divide the proceeds. This option can give both parties a clean break and financial resources to start anew. Cons: Selling a home can be time-consuming and emotionally challenging. Additionally, market conditions may affect the sale price, potentially leading to financial losses. One Spouse Buys Out the OtherPros: If one spouse wishes to keep the home, they can buy out the other spouse’s share. This option allows one party to maintain stability, particularly if children who benefit from staying in the same home and school district are involved. Cons: The buying spouse must have the financial resources to afford the buyout, which can be substantial. Additionally, refinancing the mortgage in one spouse’s name may be necessary, which could be challenging depending on their financial situation. Co-Ownership Post-DivorcePros: In some cases, divorcing couples may agree to continue co-owning the home temporarily. This arrangement can be beneficial if the housing market is unfavorable, or the children’s needs are prioritized. Cons: Co-ownership requires ongoing cooperation and communication, which can be difficult post-divorce. There is also the risk of future disputes over maintenance costs, mortgage payments, and eventual sale. Deferred Sale (Nesting)Pros: Deferred sale or “nesting” involves spouses taking turns living in the home while the children remain there full-time. This arrangement provides stability for the children and allows both parents to share in the responsibilities of the home. Cons: This arrangement requires significant coordination and ongoing communication. It is typically a short-term solution until a more permanent arrangement can be made. Some factors may be considered in determining what to do with the Marital Home, including: Financial ConsiderationsEquity and Mortgage: The home’s equity and the remaining mortgage balance will significantly impact the decision. Both parties must consider whether they can afford the mortgage, maintenance, and associated costs. Credit and Financing: Refinancing the mortgage in one spouse’s name requires good credit and sufficient income. This step is crucial if one spouse plans to buy out the other or keep the home. Children’s NeedsStability and Continuity: If children are involved, their need for stability and continuity will be a significant consideration. Keeping the marital home may be beneficial to minimize disruption to their lives. Emotional AttachmentsPersonal Value: The emotional attachment to the home can influence decisions. It’s essential to balance emotional factors with practical financial considerations. Legal AgreementsPrenuptial and Postnuptial Agreements: Any existing agreements will play a role in determining the outcome. These documents may specify what happens to the marital home in the event of a divorce. State LawsCommunity Property vs. Equitable Distribution: State laws vary in dividing marital property. There are legal process options in determining what happens with the Marital Home, including: Negotiation and MediationCollaborative Approach: Many couples resolve the fate of the marital home through negotiation or mediation. This collaborative approach allows for more flexibility and control over the outcome. Court DecisionJudicial Ruling: The court will decide if the couple cannot agree. The judge will consider various factors, including financial circumstances, children’s needs, and each party’s ability to maintain the home. Deciding what happens to the marital home during a divorce is a complex process that requires careful consideration of financial, emotional, and legal factors. Each option—selling the home, one spouse buying out the other, co-ownership, or deferred sale—has pros and cons. The decision should be guided by the best interests of both parties and any children involved, aiming for a resolution that provides stability and fairness.

July 11, 2024

Family Law

Child Privilege Attorney in Divorce: Protecting Confidentiality and Best Interests

A Child Privilege Attorney (CPA) is a legal professional appointed to protect a child's privilege, or right to confidentiality, concerning therapeutic and counseling communications. This role is vital in divorce cases where parents may seek access to the child’s therapy records to support their custody claims or other aspects of the divorce. The Role and Responsibilities of a Child Privilege Attorney Confidentiality Advocacy: A CPA's primary responsibility is to determine whether a child's confidential communications with their therapist or counselor should be disclosed in a court proceeding. A goal of the CPA is to preserve the child’s ability to speak openly without fear that their disclosures will be used against them or their parents in court. Legal Representation: CPAs represent the child in legal proceedings, arguing the issue of privileged information. They may file motions to quash subpoenas or resist the disclosure of therapy records. Balancing Interests: While prioritizing the child's confidentiality, CPAs also consider the child's overall best interests. This might involve selectively disclosing certain information if it is deemed crucial for the child’s welfare and with appropriate safeguards. Collaborating with Therapists: CPAs work closely with the child's therapist to understand the nature of the communications and determine which parts should remain confidential. Factors in determining whether or not to waive a Child’s Privilege in Divorce Encouraging Open Communication: Children are likelier to engage honestly in therapy if they know their disclosures are private. This openness is crucial for effective mental health treatment. Protecting Mental Health: Exposure of therapy records can retraumatize children, damaging their mental health and trust in the therapeutic process. Preventing Manipulation: In contentious divorces, parents might attempt to use therapy records to manipulate custody outcomes. CPAs help prevent such misuse by safeguarding privileged information. History of Abuse or Neglect: In cases involving abuse or neglect, maintaining the child’s confidentiality can be crucial for their safety and emotional well-being. However, it may be necessary to waive to inform the court of allegations made by a child in therapy. Challenges Faced by Child Privilege Attorneys Complex Legal Landscape: Navigating the legal complexities surrounding privilege and confidentiality in family law requires a deep understanding of mental health and legal principles. Parental Opposition: CPAs often face resistance from parents who believe that accessing therapy records is, or is not, in their child’s best interests. Judicial Discretion: Judges have considerable discretion in determining whether to uphold or override privilege, making the CPA’s advocacy crucial but not always determinative. Balancing Transparency and Confidentiality: Striking the right balance between necessary disclosures and maintaining confidentiality can be challenging, especially in high-stakes custody battles. An experienced Child Privilege Attorney may be appropriate in divorce proceedings, ensuring their right to confidential therapeutic communications is protected. By safeguarding this privilege, CPAs play a critical role in promoting the child’s mental health, preventing the misuse of sensitive information, and ultimately ensuring that the child's best interests remain the central focus of divorce proceedings. As awareness of this role grows, CPAs are likely to become an increasingly integral part of family law, offering children the protection and advocacy they deserve during one of life's most challenging times.

July 11, 2024

Commercial Litigation

A Divorce Checklist – Death and Bankruptcy Considerations

A substantial portion of estate and trust litigation and post-divorce enforcement litigation (“contempt proceedings”) is rooted in failures or shortcomings in negotiations or drafting during the divorce process itself. Here is a recommended “best practices” checklist of questions developed based on my nearly three decades of bankruptcy, creditors’ rights, collection and enforcement, and estate and trust litigation. This “best practices” checklist for family law (aka matrimonial law) attorneys, divorce lawyers, those contemplating divorce, and those, perhaps, already in the throes of post-divorce contempt proceedings tracks with my recently published List of “Top 5 Divorce-related Financial Protection Failures”. It incorporates lessons learned “the hard way” from potentially avoidable situations occasioned or worsened when the questions compiled here had not been considered or, if asked, ineffectively taken into account by the drafting attorneys involved in the first instance. This checklist is a practical, check-the-box application of the “Top 5 List” broken down into specific questions to be asked and answered by all involved in the divorce process. The checklist can and should be relied upon and applied (in whole or in part, depending on the circumstances) during multiple phases of a divorce proceeding. The checklist should help guide drafting considerations during negotiations of a Property Settlement Agreement when trying to avoid or limit costly equitable distribution litigation to determine how much each spouse is equitably to receive; otherwise to be measured by what portion of which assets the judge determines most appropriate after costly hearings. The checklist similarly serves to guide drafting considerations of the final divorce decree itself. Furthermore, although the checklist is intended to reduce costs and delays associated with post-divorce litigation used to hold a non-compliant spouse accountable when not adhering to one or more financial terms of the divorce, it can be equally effective during these contempt proceedings at aiding decision-making and providing both cost-saving guidance and time-saving benefits for the user. If routinely followed and effectively applied, the checklist should serve to help avoid unintended negative financial consequences while reducing future litigation and related legal fees, costs, and delays. THE CHECKLIST Insurance Notice to Provider - Has the insurance company (and/or benefits provider) been notified and / or asked about relevant policies and procedures for irrevocably assigning policy proceeds (and precluding unilateral re-designation of beneficiaries by the insured)? Beneficiary Re-designation - Have policy beneficiaries been irrevocably re-designated to identify ex-spouse (and/or child, children, or trust) expressly by name? Account Access – Has perpetual real-time account access to policy information (including, most importantly, payment status and continuing coverage) been irrevocably established? Employment Coverage - If relying upon employer-provided insurance coverage, have conditions or contingencies been established for the continuance of coverage upon termination, or if work-related coverage benefits ceases to be provided for any reason? Premium Payments - What specific protections (e.g., Irrevocable Life Insurance Trust (ILIT) or escrow) have been established to assure continuity of premium payments if the debtor-spouse refuses or is unable to pay for any reason? Real Estate Clean Title - Have you verified that there are no mechanics liens, judgment liens, or other title impediments? Premature Death - Have you analyzed and provided sufficiently for the possibility and potential impact of the premature death of either spouse? HELOC - Have you protected against additional credit extensions in addition to making appropriate arrangements for payoff or paydown? “Robbing Peter” - If an asset is to be liquidated and paid over in whole or in part, have you established consequences, contingencies, and otherwise protected against proceeds of the asset(s) being improperly disposed of, including in satisfaction of a separate financial obligation? Retitling/Disposition – Have you documented that “time is of the essence” and maximized protection of “reciprocal rights” against bankruptcy and/or failed pre-condition(s) to relinquishing, re-titling, or otherwise disposing of assets, especially real property assets? Retirement Accounts/Benefits Notice to Providers - Have all benefits managers/providers of relevant retirement accounts and benefits been given sufficient notice of all changes? Beneficiary Re-Designations - As with insurance coverages, have all beneficiaries been appropriately and irrevocably re-designated? Claim Deadlines – If in a jurisdiction with time limits on claims against a decedent’s estate (e.g., MD – 6 months), have adequate disclosures been made to assure timely action after death? Spousal Payout Elections – If applicable, have appropriate elections been irrevocably made to assure manner and means of payout after death (e.g., continuing spousal payments v. payments terminating at death)? Borrowing Restrictions – Have any outstanding loans against any retirement assets been factored in for valuation purposes and future borrowing against such assets been appropriately and irrevocably restricted? Bankruptcy Jurisdiction - Do you know what, if any, continuing jurisdiction the “divorce court” has if a bankruptcy is filed? Different Chapters - What difference, if any, would the filing of a Chapter 7, 11, 13, or “Subchapter V” bankruptcy have on your situation? “DSO’s” - Have you negotiated financial obligations regarding future PSA payments concerning whether they are subject to characterization under bankruptcy law as “domestic support obligations?” “The Automatic Stay” - Are you prepared to seek relief from the automatic stay and or pursue enforcement in bankruptcy court if a filing is forthcoming? Corporate Assets - If division and/or control of corporate assets by or between one or both of the spouses is/are to be factored, has a potential bankruptcy filing been accounted for with relevant valuation and enforcement considerations? Collectability Limitations Contempt Jurisdiction - Have you sufficiently familiarized yourself with binding local precedent regarding the scope of continuing contempt jurisdiction of the “divorce court” in the event of a bankruptcy filing? Bankruptcy Clawback/Discharge - Have you evaluated whether, and/or the likelihood of, future financial obligations might be subject to clawback or discharge in bankruptcy (and/or how the outcome/impact might differ depending on which bankruptcy chapter or sub-chapter is pursued)? Third-Party Requirements - For known assets held or controlled by third parties, has/have any specifically needed language been incorporated into the PSA, divorce decree, or contempt order to avoid later having to seek additional judicial relief as a pre-condition to third-party cooperation? Escrows/POA’s - Presuming future ex-spouse noncompliance, what, if any, limited power of attorney language and/or separate writings might be included, created, and/or escrowed to avoid, potentially altogether, future ex-spouse involvement? “Double-Duty” PSA - As a potential failsafe, have you incorporated language of present intent and otherwise satisfied necessary elements for the PSA itself to serve if/as needed as a deed, written assignment, or other ownership conveyance? (See [TWR’s “PSA as Deed”] and [TWR’s “PSA as Equitable Assignment”]

July 11, 2024

Business

Don’t Use an M&A Attorney for an Investment Banker’s Job

Most people will never experience a merger, acquisition, or other business transaction firsthand. Of those business owners who do sell their companies, few will go through the process more than once. Therefore, M&A professionals exist. When you’re embarking on the most complex and challenging business deal of your lifetime, it pays to have a few people in your corner who know what they’re doing. One of the biggest mistakes a seller can make is neglecting to build a team of experienced M&A advisors. Yet sellers frequently go to market without sufficient support. Occasionally, they attempt to handle the entire transaction themselves. This is tantamount to representing yourself in court— you’re almost always guaranteeing a victory for the other side. Similarly, when you spend less than you need to access qualified help, you can expect to get the result you pay for. Hiring an investment banker is one necessary cost sellers too often overlook. Perhaps the seller sees a banker as an unnecessary middleman, thinks their deal is too small to warrant involving one, or doesn’t understand the value the individual brings to the deal. Other times, a business owner will use an investment banker during the early stages of the transaction and dismiss them once a buyer is found. To be clear, one of the investment banker’s primary roles during a business transaction is to connect the seller to an interested buyer. Most business owners can’t simply wake up one day and find someone willing to purchase their company, which is why it’s important to work with a professional with a network and the ability to pitch the business. But your banker is much more than a matchmaker. Think of them as the overall quarterback of the deal. Like a QB, they lead the team and call the plays, always focusing on the end zone. Much of the work gets done in the huddle, so to speak. Normally, an investment banker starts by putting together a memorandum to market the business, coming up with a market strategy by analyzing the business—what it’s worth, what contracts it has in place, its revenue, and so forth. It’s the banker who understands the business better than anyone; they know the company inside and out and can see things more objectively than the owner can. Once a letter of intent has been signed—i.e. the ball has been thrown—the banker acts as a buffer between the selling principal(s) and the buyer’s people. At this point, they’ve passed the bulk of the work off to an attorney, but they remain active in the sense that they’re running interference. When lawyers are emphatically arguing for our clients’ interests, bankers are the ones keeping both parties calm, on track, and optimistic. They relay what are often heated messages (to put it mildly) in a composed and productive manner. Deals that lack this important cushion tend to flounder or implode as the parties argue and lose sight of their shared goals. I’ve worked with several sellers who didn’t realize the extent to which their bankers helped—even saved—the transaction. I’ve also had clients who linked up with buyers on their own, chose not to bring on investment bankers, and exposed themselves to intense periods of stress as a result. These clients had no one who could run interference. Worse, they created serious risks for themselves and their organizations. After signing an LOI, for instance, a buyer and seller may set an agreed-upon amount of net working capital (or operating capital) left in the business. If negotiations drag on and the seller needs more money to continue running the company in the interim, who gets to decide what kind of adjustment is fair? Who can determine how much cash the business really needs to keep in the bank? Attorneys can’t—we’re not financial people. And unlike bankers, who get paid at the end of the deal, we bill hourly. For these reasons, it’s not in your best interest to heavily involve your legal representative in any tasks better suited for your financial partner. Take it from someone who’s been there numerous times: you need an attorney and an investment banker. You wouldn’t hit the field with only a QB or only a center. Both jobs are essential, and their roles are certainly not interchangeable. Originally posted 10/3/2019, no content changes.

July 11, 2024

Labor and Employment

Employee Classification: Recent California Developments

The battle over employee classification in California has been a long one, and there is still uncertainty surrounding the future of independent contractor vs. employee classification in the state. One sector this impacts greatly is the gig economy, with companies such as Uber, Lyft, DoorDash, and Instacart awaiting a major decision that could have serious implications. The Background of Employee Classification in California Employee classification in California long relied on the Borello test, which came from a 1989 Supreme Court case. This was a multifactor case that focused on how much control the employer had over the manner and means by which the employee performed their work. However, in 2018, the Dynamx decision changed all that when the California Supreme Court adopted the ABC test for determining whether an employee was an independent contractor or an employee under California law. Post Dynamex, a worker is categorized as an employee unless the company can prove that A) the worker is free from the control and direction of the hiring entity in connection with the performance of the work; B) The worker performs work outside the usual course of the hiring entity’s business; and C) The worker is also engaged in an independently established trade or business that is of the same nature they are performing for the hiring entity. AB5 was then signed in 2019 in California, codifying the decision in Dynamex. This became law in 2020, expanding the application of the ABC test to most workers and making it even more difficult for companies to classify workers as independent contractors. The Impact on the Gig Economy Because of the nature of the gig economy, this has had a significant impact on employers within the industry. These companies relied heavily on the ability to classify their workers as independent contractors, avoiding the benefits and employment regulations that come along with employee classification (such as insurance, overtime, and minimum wage requirements). So, it is no surprise that lawsuits and ballot measures followed AB5. Many gig economy companies also sponsored Proposition 22, which was a ballot initiative that exempted app-based transportation and delivery companies from AB5. California voters approved the measure in 2020, allowing these companies to continue classifying their workers as independent contractors. Recent Developments The passage of Proposition 22 is not where this story ends. There have, of course, been legal challenges, with a judge ruling it unconstitutional in 2021. That decision has been appealed, and we are waiting for a decision from the California Supreme Court this summer. AB5 has also been challenged in the courts, with Uber and Postmates claiming the law violated their rights under the Equal Protection Clause of the state and US constitutions. However, the 9th Circuit disagreed, recently blocking their efforts to overturn the law. This latest failure for Uber in the courts means gig economy companies must rely on the California Supreme Court to uphold Proposition 22 in order to continue classifying employees as independent contractors. Broader Implications While it might seem that this only impacts companies in this space in the state of California, this does have some broader implications to consider. It highlights the real issues that exist surrounding innovation and employment law. The technology that allows these companies to operate outpaced developments in regulations and legislation governing companies and workers in this space. And while it attempts to “catch up,” the legal battles have left a great deal of uncertainty for both sides. We will be watching for the California Supreme Court’s decision on Proposition 22 that should come down in the next few months and will update on the future of employee classification in the state and what companies need to know at that time.

July 10, 2024

Labor and Employment

Texas Court Blocks FTC Non-Compete Rule: What It Means for Businesses

On July 3, 2024, a federal district court in Texas took a significant step, temporarily blocking the Federal Trade Commission's (FTC) proposed rule banning non-competes. U.S. District Judge Ada Brown for the Northern District of Texas granted the motion for preliminary injunction filed by plaintiffs Ryan LLC and plaintiff-intervenors U.S. Chamber of Commerce, Business Roundtable, Texas Association of Business, and Longview Chamber of Commerce, effectively putting the FTC’s rule on hold for the named plaintiffs. Although the stay is temporary pending the court’s final decision on the merits of the case and applies only to the movants, it signals that a permanent and nationwide injunction is likely. Background on the FTC's Non-Compete Rule As a quick refresher, in April 2024, the FTC narrowly passed a rule along party lines intended to ban future non-compete agreements and nullify most existing ones. The FTC asserted its authority to enact this rule under Section 6(g) of the FTC Act, claiming it grants the power to establish substantive rules against unfair competition. Set to take effect on September 4, 2024, the rule would prohibit all new employment-related non-competes and invalidate nearly all existing ones. Ryan LLC and others immediately challenged the rule in court on various grounds. Judge Ada Brown's Ruling on the FTC Rule Judge Ada Brown, a former President Trump appointee, ruled in favor of the plaintiffs, determining that they successfully demonstrated all the necessary criteria for a preliminary injunction: (i) a strong likelihood of winning the case; (ii) a significant risk of irreparable harm if the injunction wasn't granted; and (iii) a favorable balance of the potential harms and benefits to both parties. Judge Brown’s opinion focused on two key points: The Scope of the FTC’s Authority: The court’s determination that the FTC lacked statutory authority to enact the rule is significant, particularly considering its alignment with the "major questions" doctrine. Historically, the FTC has disclaimed such power, but Congress has not expressly granted it. The court's reasoning aligns with the recent trend of limiting agencies' authority, echoing concerns in the "major questions" doctrine. Whether the Rule is Arbitrary and Capricious: Judge Brown ruled that the rule was arbitrary and capricious under the Administrative Procedure Act (APA) due to its overbroad nature and lack of supporting evidence. The opinion noted that no state has enacted a ban as broad as the one proposed by the FTC, and the FTC failed to justify its sweeping approach or consider less disruptive alternatives. Additionally, the court agreed that the rule would cause irreparable harm to the plaintiffs' businesses and that the balance of equities favored maintaining the status quo. Current Status and Potential Developments of the FTC Rule While the injunction only applies to Ryan LLC and the U.S. Chamber of Commerce (and not its members), no entities will be subject to enforcement before the rule's intended effective date of September 4, 2024. Additionally, Judge Brown indicated that she intends to issue a final ruling by August 30, 2024, which could invalidate or permanently enjoin the rule. In the interim, the parties will further brief the merits issues and the narrow scope of the court’s order, including whether the injunction should be expanded nationwide. A separate challenge brought by ATS Tree Services LLC is pending in Pennsylvania, with a hearing scheduled for July 10, 2024, potentially resulting in a nationwide injunction 1. This underscores the potential nationwide impact of the ongoing legal proceedings. Impact on FTC's Rulemaking Authority This ruling is a significant setback to the FTC's agenda to expand its rulemaking authority and regulate labor markets. It reflects a broader trend of constraining administrative agencies following the Supreme Court's recent decision (issued June 28, 2024) in Loper Bright Enterprises. In Loper Bright, the court overruled Chevron’s deference. It concluded that courts must interpret statutes de novo, and agency interpretations are not entitled to deference. The court found that even where a statute is “ambiguous,” there is a single “best reading” of the statute that courts, not agencies, are responsible for determining. Previously, courts often deferred to agencies under the Chevron doctrine if their interpretation of an ambiguous law was reasonable. However, Loper mandates that courts independently assess whether an agency acted within its authority, regardless of statutory ambiguity. This means the Ryan court's final decision will heavily depend on its own interpretation of the FTC's statutory power. Given this new precedent, it is plausible to expect the FTC's rule may be overturned, at least in part. The business community, which has strongly opposed the rule, likely sees this as a positive sign. However, state-level efforts to limit non-competes continue, and the National Labor Relations Board (NLRB) has taken the view that the proffer, maintenance, and enforcement of non-competes generally violate the National Labor Relations Act 2. Proactive Review of Non-Competes: Alternative Strategies Businesses are advised to proactively review their use of non-competes across their organization and explore alternative strategies to safeguard their interests. These alternatives include: Non-Disclosure Agreements (NDAs) Intellectual Property Protection Non-solicitation agreements Training Reimbursement Programs Garden Leave Clauses Non-Competes Linked to Business Sales The FTC has indicated that, when properly structured, these alternatives should not violate its proposed rule. _____________________________________________ 1 ATS Tree Services, LLC v. FTC, No. 2:24-cv-1743 (E.D. Pa. 2024). 2 On June 13, 2024, an administrative law judge for the NLRB held that certain non-compete and non-solicit covenants violated an employee’s labor rights under the NLRA. See J.O. Mory, Inc., 25-CA-309577, 25-CA-336995, JD-36-24 (2024).

July 10, 2024

Business

Beyond Finances: If You Don’t Consider a Business’ Practices, You’re Missing Half the Story