Category: Business

Clear ResultsMergers and Acquisitions

Breaking Down Rollover Equity: Why Buyers Love It and What Sellers Need to Know

For many business owners, the goal of selling their company is turning their years, and often decades, of hard work into liquidity. But in some cases, retaining a stake in the company could prove to be fruitful for both the buyer and the seller. That is where rollover equity comes into play. Below is a breakdown of the benefits and risks of rollover equity, and what sellers need to know. Rollover Equity Explained The concept of rollover equity is simple. Instead of paying a seller entirely in cash, a buyer acquires 100% of the target company while allowing founders and key shareholders to retain a stake in the new ownership structure. The seller still receives some immediate liquidity at closing, exchanging the remaining portion for equity in the post-transaction business. This is certainly not a new concept and has been common in private equity transactions for some time. However, it is becoming an increasingly important tool today as buyers and sellers work to bridge valuation gaps and align their incentives in today’s more cautious deal environment. The Benefits of Rollover Equity One of the most obvious benefits of this deal structure is that it reduces the amount of cash required to close a transaction. This is a significant benefit for buyers who are motivated to preserve capital whenever possible, particularly in today’s market when financing costs are elevated, and lenders are scrutinizing leverage more carefully. Buyers do not have to fully fund a transaction with cash, but they still obtain full control of the entire company. Additionally, when founders remain involved, there is an increased confidence that the management team and employees will remain motivated and stay onboard. Continued seller participation can also help to preserve relationships, maintain operational continuity, and retain institutional knowledge after the deal closes. These non-economic factors can be critical to the company’s future success. Rollover equity can also be a tool to bridge valuation disagreements between a buyer and seller. A frequent issue that arises is a seller’s belief their business deserves a higher valuation based on its growth potential vs. the buyer’s hesitation to fully underwrite those projections in cash. A rollover structure provides a bridge for both sides to move forward despite the disconnect on valuation. The seller gets to walk away with immediate liquidity while still retaining the opportunity to benefit from the upside if the company continues to grow. That second bite at the apple can prove to be extremely valuable for a seller if the company later sells at a higher valuation. They can see returns that far exceed anything they would have generated from an all-cash transaction up front. This makes rollover equity particularly attractive for sophisticated sellers who see the opportunity to continue participating in value creation alongside the buyer. The Risks of Rollover Equity While there are many upsides to rollover equity, it is not without risk. Most importantly, sellers must fully understand what they are receiving in exchange for the portion of the sale they are not receiving in cash. The rolled equity is typically a minority stake in a buyer-controlled entity. The seller will have minimal control over future decisions, including exit timing. Therefore, the rights associated with the rollover are incredibly important and should be carefully negotiated. Rollover equity can also include some restrictions for the seller. For example, there can be mandatory hold periods, drag-along provisions, or other limitations that can affect how and when the seller can monetize their investment. The capital structure of the post-closing entity also matters. If the new entity is highly leveraged, the seller may face a very different set of risks than they did as the original owner. As with any transaction structure, a rollover transaction comes with its own set of tax considerations as well. When structured properly, rollover equity can come with the added benefit of tax deferral in certain instances for sellers, but the rules here are complex and highly dependent on deal structure. It is essential to bring in legal and tax counsel early on to ensure everything is structured appropriately and aligns with the seller’s financial goals. Rollover equity can be a highly beneficial tool for both buyers and sellers, and it will no doubt continue to be increasingly used in today’s M&A environment. But there are many considerations, especially on the sell side, that must be addressed from the start. Working with effective legal counsel throughout the process can help to reduce the risk, increase the benefits, and set up sellers for even greater success in the future.

July 6, 2026

Business

Why the Friendly PC Model Remains Critical to Healthcare Private Equity Transactions with Medical and Dental Practices

Private equity (“PE”) activity in healthcare across the United States has caused continued focus by state legislatures and enforcement agencies on the doctrines of corporate practice of medicine and dentistry (“CPOM” or “CPOD”). Notwithstanding this attention, the often-referenced “Friendly PC” model remains the optimal corporate strategy to ensure post-closing compliance with CPOM and CPOD regulations in most jurisdictions. The following identifies some key considerations for the agreement's ancillary to the purchase of the non-clinical assets by the PE company’s management services organization (“MSO”), which are commonly used to ensure compliance with CPOM and CPOD. Friendly PC Model As a general matter, the term “Friendly PC” model in PE healthcare deals most often refers to a business arrangement where a physician or dentist-owned professional corporation (“PC”) sells all of its non-clinical assets to an entity owned by the MSO (controlled by the PE firm), which then takes responsibility for the PC’s non-clinical business operations. This model complies with fundamental CPOM and CPOD legal requirements, which are designed to restrict non-physicians from owning or controlling medical practices. Such a structure prevents the PE buyer from owning clinical assets or unduly controlling the clinical operations and decision-making of the providers employed by the PC. In the “Friendly PC” structure, the parties designate a single clinical professional to serve as the sole owner of the PC post-closing. This individual is referred to as the friendly physician or dentist (“Friendly Provider”), who is then expected to cooperate with the PE buyer in accomplishing its business goals. Such a transaction requires the drafting of a series of agreements to accomplish the necessary purposes of the arrangement. Although the nature and scope of such agreements may vary slightly based upon preference and applicable state law, below is a brief description of certain key agreements, and their most necessary elements, to ensure the PC’s compliance with CPOM and CPOD laws post-closing. Management Services Agreement The Management Services Agreement (“MSA”) is entered into between the PC and the MSO, which is owned by the PE buyer. Through this agreement, the MSO is responsible for providing and arranging for certain non-clinical administrative, business support, and back-office services on behalf of the PC. The MSA will clearly state that the MSO entity will not play any role in the care of patients and will specify the limitations of the actual services to be provided so as to ensure it will not fall within the applicable state’s definition of the practice of medicine or dentistry. It is also very important that the MSA define the independent contractor nature of this commercial relationship and seeks to avoid creating a de facto partnership between the MSO and the PC.1 Overly lengthy initial contract durations, requirements for minimum operational hours per period, the ability to negotiate payor and other agreements without the PC’s consent, and compensating the MSO through a percentage of the PC’s profits are all commonly mishandled deal points that could create an unintended partnership in the eyes of a regulatory agency.2 As such, legal counsel must carefully tailor these provisions to avoid such a problematic presumption. Equity Transfer Restriction Agreement This agreement establishes a highly restrictive framework which governs the ownership and transfer of the Friendly Provider’s interests in the PC, giving the MSO near-complete control over any change in ownership. As a baseline rule, no transfer of equity—whether voluntary, involuntary, or by operation of law—may occur without the MSO’s prior written consent, which may be granted or withheld in its sole discretion. The central mechanism is a set of transfer events (e.g., death, disability, termination of services, loss of licensure, legal disqualification, divorce, regulatory issues, or breach of agreements), upon which the Friendly Provider’s entire ownership interest is automatically and immediately transferred—without notice or further action—to an MSO–designated transferee. This transfer occurs by operation of contract, is effective upon the triggering event, regardless of administrative formalities and is typically priced at a nominal $1.00. In addition, the MSO typically holds a unilateral call option enabling it to trigger a forced transfer of all equity at any time by delivering notice, which itself constitutes a transfer event and results in the same automatic $1.00 transfer to its designated transferee. Following any such transfer, the Friendly Provider is automatically stripped of all ownership, governance roles, and economic rights in the PC. The agreement further reinforces this control structure through ongoing covenants that prohibit the Friendly Provider and the PC from taking a wide range of corporate, financial, and operational actions without MSO approval, ensuring that both ownership continuity and strategic direction remain fully aligned with the MSO’s interests. Provider Employment Agreement The provider employment agreement is often viewed as the most important by medical professionals who are divesting their interest in the PC. It includes terms and conditions regarding compensation and various restrictive covenants (i.e., non-competition, non-solicitation, confidentiality) that are critical to the clinician’s relationship with the PC. Legal counsel should ensure that the employment agreement also contains specific provisions or guarantees that the clinical professionals will maintain broad autonomy in all clinical decision-making and treatment of patients post-closing.3 Under no circumstances may the PC exercise any undue control over this aspect of their clinical professional employees’ job performance, and expressly stating as such within this agreement may help the arrangement survive future scrutiny.4 Clinical Liaison Agreement Lastly, the Clinical Liaison Agreement (“CLA”), typically entered into by the PE management entity and the Friendly Provider, is a frequently used means to outsource the development and implementation of the medico-administrative services of the PC. As a licensed professional in the state of operation, the Friendly Provider is the only party legally authorized to provide such services as the supervision of clinical staff, the development of clinical policies, and the leadership of patient-related programs and initiatives. The existence of such an arrangement is therefore imperative for the post-closing clinical management of the PC. As with the other agreements, the CLA should involve a reasonable term length and consideration for the Friendly Provider’s time and effort, and it should also protect the Friendly Provider’s necessary autonomy to perform their duties as outlined therein.5 Conclusion As scrutiny of “Friendly PC” transactions continues in light of consumer and legislative concerns over the affordability of health care services, the need for proper separation of clinical and non-clinical management post-closing is likely to be more important now than in years past. As such, PE buyers and their counsel must pay close attention to these frequently overlooked ancillary agreements to ensure the truly independent nature of their post-closing relationships. 1See Warren J. Apollon, D.M.D., P.C. v. OCA, Inc., 592 F. Supp. 2d 906; and OCA, Inc., et al . Kellyn Hodges, D.M.D., M.S., et al., 615 F. Supp. 2d 477. 2Id. 3The definitions of “Practice of Medicine” and “Practice of Dentistry” vary by state, however, guidance provided by the Pennsylvania Board of Medicine provides examples of the types of rights and privileges of licensed providers that must not be interfered with or influenced by unlicensed persons or entities. (See 63 P.S. § 422.1, et seq., 63 P.S. § 120, et seq.) 4Id. 5https://journalofethics.ama-assn.org/article/physician-engagement-private-equity-firms/2025-05

June 15, 2026

Business

Why Real Estate Issues Slow ETA Deals

Most buyers expect environmental issues to be the real estate risk. In many deals, the larger risk is operational disruption. Real Estate Is Involved in Most ETA Transactions Real estate shows up in the vast majority of lower middle market transactions in some form. According to the 2025 Small Business Credit Survey published by the Federal Reserve: approximately 59% of operating businesses with employees operate from leased facilities approximately 17% operate from owned facilities approximately 17% primarily operate from a residence or without a dedicated operating facility That means roughly 83% of entrepreneurship through acquisition transactions involve some form of real estate or occupancy issue. In many deals, the primary issue is not ownership of the property itself. It is whether occupancy, control rights, lease assignment provisions, lender requirements, zoning, or permits could interfere with the business continuing to operate after closing. Those risks often become the primary real estate issues affecting the transaction. Most Buyers Initially Focus on Environmental Risk Environmental exposure absolutely matters. Particularly in: manufacturing industrial logistics automotive fuel-related operations older commercial corridors Phase I and Phase II reports remain critical diligence tools. But many search funders, independent sponsors, and ETA buyers do not place enough weight on operational interruption risk. While the business may technically exist independent of the property, operationally, it often does not. Location Becomes Part of the Business Most of these businesses are highly dependent on their physical operating environment. Examples include: machine shops with specialized electrical infrastructure distributors dependent on loading access and trucking routes contractors relying on outdoor storage rights restaurants dependent on parking and liquor licensing healthcare operators dependent on permitted use manufacturers operating under grandfathered zoning protections The issue is not simply whether the business can move. The issue is: cost of relocation operational downtime customer disruption employee retention permitting risk lender reaction transition timing Many ETA buyers do not fully appreciate this until diligence deepens. Lease Problems Often Surface After LOI One issue that repeatedly appears in ETA deals is whether the business can continue occupying the property after closing under the existing lease arrangements. Many buyers initially assume that the lease will (and can) transfer automatically at the time of closing. That is often incorrect. Most commercial leases contain assignment restrictions, consent requirements, or change-of-control provisions that must be examined carefully during diligence. Buyers need to identify: anti-assignment clauses landlord consent requirements change-of-control provisions expired lease terms undocumented extensions side agreements reflected only in emails use restrictions relocation rights held by landlords personal guarantees tied to the seller While the business operated successfully under these arrangements for years, a transaction introduces scrutiny, diligence, lender review, and operational friction. Lenders Underwrite Real Estate Issues Aggressively Occupancy stability becomes especially important in financed transactions. Particularly: SBA-backed deals owner-occupied industrial acquisitions cash flow sensitive businesses location-dependent operations Lenders often focus heavily on: remaining lease term renewal rights assignability ownership structure related-party lease economics appraised value environmental exposure zoning compliance A business with strong EBITDA but only 18 months remaining on a lease can quickly become a financing issue. Especially if the landlord has leverage during the closing process. Owned Real Estate Creates a Separate Transaction (and Separate Issues) Buyers often assume owned real estate simplifies the acquisition. In reality, it frequently creates a separate parallel transaction with its own diligence process, timeline, costs, and risks. The buyer must now perform diligence on both the operating business and the real estate itself, including: title survey and boundary issues easements zoning environmental exposure permits deferred maintenance tax exposure utility access stormwater compliance shared access arrangements The ownership structure also becomes critical, with many ETA deals using separate entities for the business and real estate. For example: one LLC owns the operating business another entity owns the real estate the operating company leases the property from the real estate holding company That structure often creates cleaner liability separation, financing flexibility, estate planning opportunities, and long-term control over the property. The larger problems often appear when the business and property were never properly separated in the first place. Many older lower middle-market businesses operate under informal ownership structures where: the seller personally owns the property family members own portions of the real estate title ownership differs from operational control there is no formal lease occupancy economics were never documented properly related-party arrangements evolved informally over decades That creates a very different set of diligence and execution risks. Buyers now need to examine: who actually owns the property whether all owners are participating in the transaction whether any family members must consent whether the operating business has formal occupancy rights whether market rent materially changes EBITDA whether lender underwriting changes once rent is normalized whether personal use or mixed-use issues exist whether title, tax, or succession issues affect the property whether post-close disputes could arise around occupancy or control Real Estate Distorts EBITDA More Than Buyers Expect Normalized occupancy costs also frequently change the underwriting. This issue regularly shows up in entrepreneurship through acquisition transactions, causing the business to appear more profitable because the seller owns the building. The company may operate with: below-market rent no formal lease favorable related-party occupancy terms deferred maintenance underreported capital needs Once the buyer normalizes rent, maintenance, taxes, insurance, market occupancy economics, and other carrying costs, the cash flow can compress quickly. That affects: leverage availability DSCR calculations valuation purchase price expectations post-close cash needs This is particularly important in manufacturing, warehouse, automotive, and hospitality acquisitions. Zoning Problems May Remain Hidden Until Diligence It can be a misconception to assume: “The business already operates there, so zoning must be fine.” Not always. A lack of zoning compliance can significantly disrupt operations. Businesses sometimes operate under: grandfathered nonconforming uses historical variances undocumented expansions expired permits improper outdoor storage occupancy inconsistencies signage violations prior approvals tied to historical ownership A transaction can trigger: new permit review lender diligence insurance underwriting review municipal scrutiny updated inspections The business may have operated without issue for years, but that does not mean the use remains protected post-closing. Real Estate Risk Can Show Up Everywhere Real estate issues quickly spread into: financing operations integration employee retention transition planning insurance working capital timing of closing The issues then become larger than the property itself. Real estate issues are most prevalent in lower middle market acquisitions where: documentation evolved informally occupancy arrangements were relationship-driven operational processes were never built for institutional diligence In these ETA deals, the answer to the real estate question ultimately controls: “Can the business continue operating the same way immediately after closing?”

June 10, 2026

Mergers and Acquisitions

When the Deal Gets Personal: The Emotional Inflection Points of Selling a Business

Selling a business is largely viewed as a financial transaction shaped by valuation, structure, diligence, and closing. However, for founders and owners, selling a business is also an emotional journey that can be a highly stressful event. That stress can be compounded when a corporate attorney is brought in late in the process when many sellers have already experienced the early and most precarious stages of the deal. Many sellers work with an investment banker to take the company to market, vet buyers, and there may even be a letter of intent (LOI) on the table before an attorney is brought on board. While the seller feels they are making progress, from a legal and strategic standpoint, this early stage is where complexity and stress begin to escalate and legal counsel is critical. We have discussed the importance of bringing in legal counsel early in the process in multiple posts, and that cannot be emphasized enough. Below, we examine the most stressful components for sellers in any deal and how bringing in legal counsel early can help to ease the burden. Letter of Intent The LOI is one of the earliest inflection points in the deal process. Sellers often underestimate its significance because they see it as non-binding on economic terms. But this is a false sense of flexibility because exclusivity and time restrictions are binding. Once that LOI is signed, the seller is essentially off the market for a determined period and cannot engage in discussions with other interested buyers. This is where leverage begins to shift from the seller to the buyer. The buyer now has two things that are very valuable: time and access. On the other side, the seller is now increasingly invested, both financially and emotionally, in making the deal happen. It is now harder for the seller to walk away from the deal, even if circumstances change. Diligence The leverage shift becomes more pronounced when the deal enters the diligence stage. Buyers are highly disciplined as they approach this phase of the transaction, particularly when they are sophisticated financial sponsors. Diligence is not about buyers just confirming what they have been told, but rather testing assumptions, looking for weaknesses, and then recalibrating valuation based on their findings. It is common for buyers to reassess price or deal structure because of what is uncovered during diligence, and for sellers who entered the process with a clear expectation of value, that can be jarring. The business they have spent years or even decades building is now being evaluated through a different lens. Consistent Performance Another layer that multiplies the pressure on the seller is the expectation that the business continues to perform at the same level throughout the entire process. Entering negotiations to sell does not equate to a pause in operations. It is simply a process that runs parallel to day-to-day operations. Sellers must manage diligence requests, respond to buyer questions, and engage with all their advisors, all while effectively running the company. They cannot afford for performance to dip, even for reasons that have nothing to do with the transaction. That can lead to a reason for renegotiation, with buyers adjusting terms, implementing additional protections, or even revisiting the valuation entirely. This creates constant tension for the seller who is trying to execute the deal and simultaneously maintain the underlying business. Delayed Engagement of Legal Counsel When a seller brings in legal counsel later in the transaction, it can feel disruptive at first. This is because the job of an attorney is to identify and address risks, clarify what has already been agreed to, and ensure that the documents accurately reflect the intended deal. If they are not involved from the jump, they may have to revisit assumptions or unwind understandings that developed earlier in the process. This can feel like friction or a change in direction for sellers, and that can be avoided when counsel is engaged from the start. The issues become even greater when the buyer is a private equity (PE) firm. These repeat players operate with well-established playbooks and experienced deal teams. This is in stark contrast to a first-time seller who sees this as a once in a lifetime event. For a PE firm, this is just a routine transaction. The imbalance this creates can heighten the emotional stakes, particularly when discussing complex deal components. The Personal Dimension The personal dimension of the deal overlays everything. For a seller, their business represents years of work, relationships, and their identity. Their company is not just an asset they are selling; it is often their life’s work. Layer in concerns about their employees, customers, and their legacy, and the personal connection to the business complicates everything. Sellers often carry the weight of the transaction on their own, while they must continue to lead their company, One other very important reality for sellers is that the deal is not done until it is closed. It is easy to get excited and assume that signing an LOI or moving through the diligence process means the outcome is assured. But the truth is that transactions can, and do, change late in the process. Terms evolve, issues emerge, and sometimes, deals fall apart. It is critical to maintain perspective and discipline and attempt to put emotions to the side. The bottom line for sellers is that every transaction must be approached with preparation and support from the start to minimize the significant stress that comes with every stage. Bringing in skilled legal counsel very early in the process can alleviate that stress and help sellers to not only maximize value, but also bring clarity to the many complexities of a sale, resulting in a deal that truly reflects the seller’s goals.

June 1, 2026

Business

Post-Close Alignment in Lower Middle Market M&A: Where Deal Stress Begins to Fracture

Most sellers and buyers in lower-middle-market M&A, including search funds, entrepreneurship through acquisition (ETA), and independent-sponsor transactions, begin to suffer from deal fatigue and welcome the post-closing phase of a business acquisition or M&A transaction. No more due diligence, no more negotiations, no more redlines. However, in many cases, the post-close phase is fertile ground for additional disputes to emerge. Most post-closing friction in lower-middle-market M&A deals is not caused by something that was absent from the deal. To the contrary, it is actually related to the negotiated documents governing the relationship between seller and buyer in the post-close transition phase. Consulting agreements, employment agreements, and corporate governance documents in rollover equity transactions seek to govern the relationship, but the relationship is still new in this phase. The parties are experiencing, for the first time, what it is like to work together after the change in dynamics (seller-owner to exited owner; buyer with funding to operator managing debt service and performance expectations). In this example, the seller rolled equity in the transaction and was now an equity holder in the buyer's platform company. The post-closing issues did not stem from a missing provision, but from ambiguities that existed across multiple documents that were meant to align and work together: seller notes, management agreements, and governance documents were all in play and created more confusion than clarity. That pattern is more common than most buyers expect, particularly in search fund, entrepreneurship through acquisition (ETA), and independent sponsor deals where post-close roles and governance tend to be more fluid. The LOI to Close Gap in M&A Transactions Most of these issues are not created at closing. They are created in the window between LOI and signing. At LOI, the parties align on high-level economics and general expectations: The seller will stay involved The business will transition smoothly Equity will keep everyone aligned in the case of rolled equity, or amounts due pursuant to the seller note will incentivize cooperation But those concepts get translated into separate documents depending on the deal: Employment agreement Consulting agreement Operating agreement Purchase agreement Each document answers a different question. Very few processes force those answers to be reconciled into a single operating model. That is where the gap forms. By the time you reach closing, the documents are “complete” but not always aligned. Where Post-Closing Issues Show Up in Business Acquisitions Employment Terms in Post-Closing Transition Buyers often assume that key individuals, particularly a selling owner transitioning into an operating role, will continue “as expected.” The employment agreement is where that expectation either becomes a reality or breaks down. The most common issues include: Role definition is too broad or not tied to actual authority Termination provisions do not reflect how performance issues will be handled Compensation structures do not match the deal model Example: A seller stays on post-close in a senior operating role (e.g., general manager) under a two-year agreement while the buyer installs its own CEO or operating partner. The buyer expects to reshape reporting lines and decision-making authority over time. The agreement, however, includes strong severance protections and defines material changes to duties or authority as “good reason.” Six months in, the buyer begins shifting responsibilities to its operating partner. The seller asserts “good reason” and triggers severance or other protections, despite the buyer viewing the changes as part of the planned transition. Nothing is technically wrong in the document. It just does not reflect how the buyer intended to transition control of the business. Consulting Roles and Transition Services Agreements Consulting arrangements are often treated as secondary or low-risk. In practice, they can drive real execution outcomes. This is especially true in customer transition and institutional knowledge transfer. Where this tends to go wrong: Scope of services is loosely defined Time commitment is not specified Compensation is not tied to outputs Example: A seller agrees to a 12-month consulting arrangement to support transition. The agreement references “reasonable availability” but does not define hours, deliverables, or response expectations. Post-close, the buyer expects active involvement in customer introductions and onboarding. The seller views the role as limited advisory support that can be provided from a remote location and not on-site. The result is predictable. The buyer feels unsupported. The seller believes they are complying with the agreement. Again, nothing is broken in isolation. The expectations were never aligned. Rolled Equity and Post-Close Governance Rolled equity is typically framed as a tool to align the parties in furtherance of a more profitable enterprise. In practice, it can be alignment in concept only, not in execution. Where this tends to go wrong: Different expectations around liquidity timing Limited clarity on governance rights Misunderstanding of distribution mechanics Example: A seller rolls 20% of proceeds into the new structure. The buyer plans to reinvest cash flow into growth and limit near-term distributions. The seller expects periodic cash flow similar to how they operated pre-sale. The operating agreement permits discretion on distributions, but the practical application of that discretion was never aligned. This is not a legal defect. It is an operating mismatch that surfaces quickly once capital allocation decisions begin. Why Post-Closing Misalignment Occurs in M&A Deals During the deal process, these items are negotiated in parallel: Purchase agreement Employment agreements Consulting agreements Equity and governance documents Each document may be internally consistent, but the following question should be asked: Do these documents, taken together, reflect how this business will actually be operated on day one? More specifically: Do they clearly define what the seller is required to do, what authority they retain or lose, how they are compensated for that role, and what happens if those expectations change or break down? If the answer to those questions is unclear, the issue is already embedded in the deal. Practical Considerations Pre-Close in Lower Middle Market Transactions This is almost always easier to address before closing than after. In practice, a strong lower-middle-market post-close package tends to do six things: Define the role with objective deliverables. Move beyond titles. Specify outputs, metrics, and decision rights that tie to how the business will actually be operated. Clearly classify the relationship. State whether the seller is an employee, consultant, or board-level advisor. Blurred status tends to create both operational and legal ambiguity. Precisely frame “cause” and “good reason.” If the buyer retains flexibility to change duties, reporting lines, compensation, or authority, that flexibility should be clearly bounded. Well-defined “cause” and “good reason” concepts are what translate flexibility into enforceable expectations. Separate consulting economics from deal economics. Consulting fees should stand on their own unless the parties intentionally link them to purchase price or earnout mechanics. Unintended overlap often creates disputes about what is being paid for performance versus transition support. Build explicit consequences for disruption. If authority is stripped or termination occurs outside the expected framework, the documents should address the outcome. That can include tolling, acceleration, deemed achievement, or extension concepts tied to equity or earnouts. Preserve a practical enforcement path. Rights are only useful if they can be exercised. Escrow access, information rights, expert determination procedures, and specific performance provisions tend to make these arrangements function in practice. Closing Thought on Post-Closing Risk and Deal Execution These are not technical refinements. They determine whether the post-close relationship functions when conditions change. Most post-closing issues do not come from a single broken provision. They come from small inconsistencies across multiple documents that were never forced to align into a single operating framework. If you are under LOI or in diligence, this is typically the window to fix that alignment without disrupting the deal. After closing, you are no longer interpreting intent; you are operating within the structure you drafted. If you are working through this in a live deal, step back and ask: Do these documents, collectively, dictate how decisions get made, how the seller participates, and how economics actually flow? If not, then the risk is not theoretical. It is already built into the deal.

May 29, 2026

Business

Virginia Reshapes Franchising with Ban on Post-Term Non-Competes

Franchisors with Virginia locations should prepare to revise their franchise agreements and Virginia-specific disclosure materials. Beginning July 1, 2026, Virginia law will prohibit most post-termination non-compete provisions in covered franchise agreements and will require those agreements to be governed by Virginia law. For franchisees, the amendments create greater post-exit flexibility and reduce the ability of franchisors to rely on out-of-state governing-law clauses to avoid Virginia’s statutory protections. The practical message is straightforward: franchisors should review Virginia-facing templates, renewal and amendment practices, confidentiality and trade secret protections, and enforcement strategies well before making any new offer, sale, renewal, extension, or amendment for a Virginia location on or after the effective date. Implications for Virginia Franchisors and Franchisees These changes matter immediately for drafting and compliance. A franchisor that continues to use a standard national form for Virginia deals without modification risks including provisions that will no longer be permitted once the new law takes effect. Agreements entered into before July 1, 2026, are not automatically displaced, but renewals, extensions, and amendments on or after that date may trigger the new requirements, making it especially important to review not only new-deal documents but also legacy agreements that may soon come back into circulation. Public commentary following the legislation has also noted guidance issued on April 14, 2026, by the Virginia State Corporation Commission’s Division of Securities and Retail Franchising regarding updates to franchise disclosure materials and Virginia addenda, underscoring that compliance will require attention not just to contracts but also to disclosure practice. How Virginia’s New Franchise Non-Compete Law Affects Franchise Agreements The amendments to Virginia’s Retail Franchising Act, enacted through House Bill 69 and the companion Senate Bill 240, apply to franchises that require or contemplate a place of business in Virginia, a concept broad enough to reach more than traditional brick-and-mortar outlets and potentially many service concepts operating in the Commonwealth. Effective July 1, 2026, the law makes it unlawful to offer or enter into a covered franchise agreement that restricts the franchisee’s right to engage in the business of offering, selling, or distributing goods or services at retail after termination or expiration of the franchise agreement. Just as significantly, covered franchise agreements must now be governed by Virginia law, preventing franchisors from selecting another state’s law in an effort to sidestep Virginia’s franchisee protections. Virginia Franchise Non-Compete Exceptions The statute includes a narrow exception when a franchisee voluntarily sells the franchise at a mutually agreed price, whether to a third party or back to the franchisor. In that setting, the franchisor or the buyer may require the selling franchisee to agree to a non-compete that is binding for up to two years after the sale. Outside that sale context, however, post-term non-compete restrictions in covered Virginia franchise agreements are no longer permitted. The law is also expressly prospective: contracts entered into, extended, or modified on or before June 30, 2026, remain unaffected, but activity on or after July 1, 2026, may bring an agreement within the amended statute’s reach. The Business Impact of Virginia’s Franchise Non-Compete Ban and Compliance Steps for Franchisors Taken together, the amendments materially rebalance franchise relationships for Virginia locations in favor of franchisees by eliminating most post-termination non-competes and requiring Virginia law to govern covered agreements. That governing-law requirement may prove especially consequential, because it reduces the usefulness of contract provisions that previously might have directed disputes toward more franchisor-friendly legal standards. It also means that franchisors evaluating renewals, transfers, terminations, and system enforcement in Virginia will need to assess those decisions against Virginia’s franchise-specific statutory framework. For franchisors, the likely response will be to strengthen other forms of system protection that do not depend on a post-term non-compete. Confidentiality provisions, trade secret controls, non-solicitation language where appropriate, access limits on customer data, tighter operational safeguards, and clearer brand-transition requirements may all take on greater importance. The statute does not prevent a franchisor from pursuing monetary remedies when a franchisee breaches contractual obligations during the term, so careful drafting around in-term defaults, de-branding obligations, liquidated damages, and post-termination transition steps may become more important than ever. The new law may also influence how franchisors think about renewal rights in Virginia. If a former franchisee cannot be restricted from competing after expiration in most circumstances, franchisors may revisit whether renewal should remain automatic or broadly available, and whether Virginia-specific renewal provisions should be adjusted to reflect the changed competitive landscape. For franchisees, by contrast, the law creates additional bargaining leverage and a more realistic ability to continue in business after the franchise relationship ends, provided they do so without violating enforceable contractual duties that survive termination. More broadly, Virginia’s action may be an early indication of where franchise regulation is heading in other jurisdictions. Franchisors operating nationally may therefore want to treat these amendments not as an isolated state-law issue, but as a signal to review their broader contract architecture and protective covenants across the system. For now, however, the immediate takeaway is clear: any franchisor with Virginia-facing agreements or pending registration materials should act promptly to align its documents, disclosures, and operational protections with the Commonwealth’s new rules before July 1, 2026.

May 18, 2026

Mergers and Acquisitions

First Time Buyers: Avoiding Analysis Paralysis

For first time buyers, the diligence phase of an acquisition can be overwhelming. Every document review, identified risk, and unanswered question, can lead to hesitation, and hesitation can quickly turn into something known as “analysis paralysis.” This can be a dangerous place for a transaction as it leads to a loss of momentum or even loss of the deal entirely. It is important for first time buyers to understand that no deal is without risk. You cannot eliminate risk entirely, but you can understand it, quantify it, and allocate it appropriately. When first time buyers recognize this reality early in the process, they are far more likely to move through the diligence process with confidence and ultimately have a successful closing. Below we look at some of the ways first time buyers can help to avoid analysis paralysis and build in the kind of protections that will allow them to move forward with ease. Bring in Advisors Early One frequent error among first-time buyers is delaying the engagement of experienced advisors, especially legal counsel. Legal counsel should be involved before the Letter of Intent (LOI) is signed, as their early participation enables the deal team to identify key issues, recognize potential risks, and structure the transaction to align price with risk effectively. Early involvement of advisors ensures that, upon reaching the diligence stage, the team is prepared to execute a strategy that has been thoughtfully designed from the outset, rather than developing one mid-process. Shifting Risks To allocate certain risks from the purchaser to the seller, it is essential to include precise representations and warranties, along with unambiguous indemnification clauses. When concerns arise, such as outstanding liabilities or matters identified during due diligence, targeted indemnities can significantly strengthen the buyer's protection. These safeguards enable buyers to move forward with a transaction even when not every issue has been conclusively resolved. Financial Structuring The financial structure of a transaction is equally significant as the inclusion of contractual safeguards. Transactions may be designed to incorporate financial protections for the buyer, such as escrow arrangements, holdbacks, or promissory notes. Additionally, earnouts provide further protection, particularly in situations where future company performance remains uncertain. By linking a portion of the purchase price to post-closing results, buyers can mitigate the risk of overpayment while enabling sellers to realize their preferred valuation. Deal Momentum One of the most important considerations for first time buyers is maintaining deal momentum. Conditions can shift quickly as transactions progress from market conditions to financing terms to business performance. If the diligence process is stalled, it allows more time for these conditions to shift, often leading to increased risk or erosion in value. When sellers lose confidence in the transaction, they could begin to entertain a competitor’s bid. Shifting conditions could also lead to a need for price adjustments or renegotiation of other terms. This is exactly where advisors prove invaluable. They can help buyers to distinguish between those issues that need immediate attention and are true red flags, as opposed to those that can be addressed through deal structure. Advisors can instill the kind of confidence in first time buyers that allows deals to move forward, even if every variable is not perfectly resolved. For those buyers entering the M&A process for the first time, the key is not to avoid risk, but to manage it intelligently. With the right team and a disciplined approach to maintaining momentum, buyers can avoid analysis paralysis and position themselves for a successful closing.

May 4, 2026

Business

Maryland Franchise Reform Act Passes

The Maryland General Assembly has enacted, by overwhelming majorities, the Franchise Reform Act (Senate Bill 415 & House Bill 730), marking the first significant changes to the Maryland Franchise Registration & Disclosure Law (the “Maryland Franchise Law”) since its enactment in 1981. Governor Moore is expected to sign the legislation into law shortly, and it will become effective on October 1, 2026. The House sponsor and primary driver of the legislation, Delegate Marc Korman, introduced the bill resulting from numerous constituents who had raised concerns about the franchise registration process in Maryland, concerns shared by franchisors nationwide. However, while part of the law will encourage streamlining the Maryland franchise sales registration process, it also provides changes that will be helpful to Maryland franchisees and Maryland-based franchisors. Having focused my practice on franchise law in Maryland for more than 25 years, I was privileged to be asked by Delegate Korman to work closely with him and his staff on the drafting and revising of the legislation, which included conducting workgroup focus meetings with members of the Maryland State Bar Association (“MSBA”) to gather feedback, and testifying on behalf of the MSBA in favor of the legislation multiple times throughout 2025 and 2026. The Maryland Franchise Law protects people considering the purchase of a franchise from being misled or under-informed when deciding whether to buy. The law requires franchisors to prepare a prospectus (called a “Franchise Disclosure Document” or an “FDD”) detailing a wide variety of information and submit it to the Securities Commissioner, who is an officer with the Maryland Office of the Attorney General (the “OAG”), and obtain that agency’s approval to sell franchises in Maryland. That approval, called registration, must be renewed each year in which the franchisor continues to sell franchises to Maryland residents or for the operation of the franchised business in Maryland (collectively, “Maryland Franchises”). Until now, the law has solely addressed the franchise sales process, rather than the ongoing relationship between the franchisor and the franchisee. The Maryland Franchise Reform Act does the following: For the Benefit of Franchisors Generally Following the bill’s initial introduction and passage by the House of Delegates during the 2025 session, the Securities Commissioner established a pilot program intended to expedite franchise registration renewals. The approved law requires the Securities Commissioner to continue the pilot program and to report to the legislature in 2031 on the program’s results, as well providing data on other aspects of the registration process, and an analysis of how Maryland’s exemptions from registration for experienced franchisors compares with those of other states that require registration before sale of a franchise. For the Benefit of Maryland Franchisors The law limits private parties who can sue a franchisor for violation of the Maryland Franchise Law solely to Maryland franchisees. This will eliminate the ability of out-of-state franchisees to use the statute as a weapon in disputes with franchisors that are or were headquartered in Maryland, which has been a deterrent to franchising from Maryland as compared to nearby states. For the Benefit of Franchisees Consistent with the Maryland Franchise Law’s purpose, parts of the law will benefit franchisees. Specifically: For the first time, the Maryland Franchise Law addresses the imbalance of power between franchisees and franchisors within the ongoing relationship, by prohibiting a franchisor from restricting or inhibiting Maryland franchisees from associating with other franchisees within their brand for the franchisees’ common benefit “for any lawful purpose” — which could include collectively raising grievances with the franchisor for the franchisees’ mutual benefit. Maryland franchisees will have the right to sue in Maryland courts for injunctive relief and damage suffered, if the franchisor violates this prohibition. This provision is similar to “free association” laws passed in several other states, including California and Illinois. The time during which a franchisee may bring a private claim for violation of the law’s registration or disclosure provisions has changed in a manner that benefits certain franchisees. Franchisees will now have until the earlier of four years from buying the franchise rights or two years after the date the franchise opened to the public. The limitations period was three years from the date the franchise rights were purchased, regardless of when the franchised business opened. The advantage will be for retail franchises that often take two years or more from buying the franchise to open due to challenges in securing an acceptable site and constructing the franchise, since those owners then will have time after opening to determine the viability of their investment and whether the franchisor violated the Maryland Franchise Law in selling the franchise. For franchises that open within a short time of purchasing the rights, the judgment of the MSBA and the legislature was that two years from opening is sufficient for a franchisee to make that determination and commence a lawsuit.

April 30, 2026

Business

Strategic Equity Partners: Expertise vs. Governance Friction

In many platform acquisitions (particularly in search funds, entrepreneurship through acquisition (ETA) transactions, and independent sponsor deals), adding a “strategic equity partner” is framed as a clear positive. There are real benefits like additional capital, operating experience, lender credibility, and often a higher probability of closing. The issue is less about whether to add a partner and more about when and how that partner is introduced. When a strategic partner is brought in after the LOI is already signed, the timeline to negotiate the governance framework is compressed. The narrative and excitement at that stage remain focused on upside, while the governance implications of adding another decision-maker are pushed into later negotiations. The LOI-to-close window is compressed, and incentives shift toward getting the deal done. As a result, governance is frequently finalized under pressure rather than designed deliberately. The impact is rarely economic at the outset. It shows up in execution. As additional partner approvals and consent rights are layered in, decisions that were previously within the operator’s control now require alignment across multiple stakeholders. More stakeholders mean more approvals, and more approvals tend to slow the process. That friction is not always visible during the transaction itself. It becomes more apparent in the first 100 days post-close, when the business needs to move quickly, and the governance structure does not support the pace that was underwritten. This dynamic is more pronounced in roll-ups, including those executed through search funds, ETA platforms, and independent sponsor structures, where speed and repeatability drive returns. Even modest governance drag can change outcomes. A structure that is directionally sound but operationally constrained can often underperform a simpler structure that can execute consistently. There is a counterpoint: more deliberate governance can lead to better decisions. The tradeoff between decision quality and execution speed should be explicit rather than assumed. What “Strategic” Usually Signals Introducing a strategic partner at LOI often reflects a gap in the team rather than a pure enhancement. This is especially common in search fund and independent sponsor transactions, where the operator is building infrastructure in parallel with executing the acquisition. The framing is additive, but the underlying driver is frequently a need to solve for something that is not yet fully built into the platform. This dynamic also mirrors a broader structuring question: where strategic partners sit in the equity stack—at the holdco or portfolio level—can materially impact governance and decision flow, not just economics. In many cases, the platform relies on capabilities that are still developing. Integration experience is a common example. The roll-up model assumes that acquisitions can be absorbed efficiently, but that capability is often unproven at the platform stage. Industry-specific operating knowledge may also be limited, particularly where the operator is entering a new vertical or scaling beyond prior experience. Systems and reporting infrastructure tend to lag the ambition of the strategy, creating a mismatch between what is modeled and what can be executed. The natural response is to introduce a strategic partner to bridge that gap. Lender dynamics often reinforce the decision. In leveraged transactions, the team is underwritten alongside the asset. A strategic partner can strengthen that narrative by adding perceived institutional support and a track record that lenders recognize. In some cases, this improves terms or increases certainty of a close. The partner effectively becomes part of the credit story, not just the equity stack. Integration bandwidth is another driver. Roll-ups assume the ability to absorb add-ons quickly, often without a fully built-out operating platform. A partner is expected to support that integration planning and post-close execution, thereby reducing execution risk. There is also an element of risk sharing. Particularly in first platform deals or more aggressive investment theses, bringing in a partner spreads exposure and introduces another perspective if/when performance deviates from plan. None of this is inherently problematic. In many cases, it is a rational response to real constraints. The consistent consequence, however, is that the partner brings governance, and governance changes how the business operates. The key is to enter the deal with a clear understanding of how that governance will function in practice. The below demonstrates a typical board structure in traditional search fund models. You can explore the different models and board structure further here: https://tinyurl.com/2rh74bk2 Where Friction Shows Up As briefly mentioned above, the friction impact appears in decision-making. As additional consent rights are layered in, more parties must agree before action can be taken. The underwriting model may assume speed and autonomy that no longer exists once governance is expanded. Board composition is often where this dynamic becomes real, because it determines who actually has the ability to approve or block decisions. A balanced board on paper can function as a checkpoint in practice once quorum and voting thresholds are applied. If control is not clearly aligned with the operating model, the board shifts from oversight to gatekeeping. Decisions that would otherwise be routine begin to require formal coordination, special meetings, and sometimes even input from professional advisors representing various stakeholders. Protective provisions compound the effect. In practice, these are the provisions that designate certain actions as “reserved matters” requiring supermajority or unanimous consent at the board or investor level. Common examples include: incurring or refinancing debt, approving capital expenditures above a threshold, deviating from the approved budget or business plan, issuing additional equity, or entering into material contracts or acquisitions. Each of these approvals is reasonable on its own. When each step requires a supermajority or unanimous sign-off, the process shifts from operator-led execution to coordinated approvals across multiple stakeholders, which slows the cadence of decision-making. The issue is not the existence of these rights, but how frequently they are triggered in the normal course of operating the business. Budget approvals can create the same constraint. When budgets require approval and variance thresholds are tight, routine adjustments turn into approval processes, limiting management’s ability to respond in real time. Roll-ups rely on speed, and competitive processes — particularly in lower middle market ETA and independent sponsor deals — tend to reward buyers who can move quickly with certainty. If each add-on requires layered approvals, the platform becomes less competitive. Opportunities that fit the thesis may still be identified, but the ability to act on them is constrained by structure rather than strategy. This is why the friction becomes most visible in add-on acquisitions, where speed is often the deciding factor in winning the deal. Management decisions can also migrate from operator discretion to investor approval. Hiring, compensation, and incentive alignment become slower to execute. Over time, this affects the quality and responsiveness of the team, particularly in periods where rapid adjustment is required. Deadlock and Forced Outcomes As additional stakeholders are introduced, disagreements become more likely. In many structures, those disagreements ultimately point parties toward formal deadlock mechanisms. These can include buy-sell arrangements (often structured as “Russian roulette” or “Texas shootout”), put/call rights, forced sales or buyouts, or redemption rights. These mechanisms are designed to break impasses, but they can be outcome-determinative and, in some cases, harsh to one side. A forced buyout may require a sponsor or the company to purchase an equity stake at a defined price or formula, which can create meaningful cash flow strain at the exact moment the business needs capital to execute. Alternatively, a party may be compelled to sell at a time or valuation that does not align with the original thesis. The key point is not that these provisions should be avoided. It is that once disagreements arise, the path to resolution is often binary and financially significant. If those dynamics are not considered upfront, governance can shift from a tool for alignment to a mechanism that forces outcomes under pressure. Why It Matters More in Roll-Ups Single-asset acquisitions can tolerate some governance friction because the operating model is relatively stable. Decisions are fewer in number and less time-sensitive. In that context, additional oversight may be manageable. A roll-up operates differently. The model depends on pace, repetition, and the ability to act decisively across a sequence of opportunities. Each add-on introduces new variables, and the platform must be able to respond quickly to integrate, optimize, and move forward. When governance introduces multiple layers of approval and frequent investor involvement in operational decisions, the strategy becomes harder to execute in practice. Decisions can still be made, but not at the speed required to maintain momentum. At that point, governance directly affects outcomes and is difficult to unwind without renegotiating core terms. The graphic below shows a sample board composition after numerous acquisitions. Note the increasingly limited decision-making power of the operator. Decision Rights to Resolve Early If a strategic partner is introduced around LOI, whether it be in a search fund, ETA, or independent sponsor context, decision rights should be aligned with how the business will operate in practice. Board control at closing needs to be explicit and consistent with the intended operating model. Ambiguity at this stage tends to create friction later. It is also worth recognizing why these protections exist. Investors are seeking to protect capital and, in many cases, bring real experience that can improve outcomes. A well-constructed board can provide discipline, identify risks early, and prevent decisions that would otherwise impair value. The goal is not to remove oversight, but to calibrate it to support execution rather than impede it. Management authority should allow day-to-day decisions without repeated escalation. The distinction between strategic oversight and operational control needs to be clear in both concept and documentation. Add-on acquisition parameters should be defined in advance, so execution does not depend on real-time approvals. Debt capacity should align with the expected capital strategy rather than restrict it. Budget processes should allow for adjustment as conditions change, rather than lock the business into a static plan. Management should retain sufficient control to build and adapt the team required to execute. Deadlock provisions should be evaluated based on how quickly they can resolve disagreement, not simply how balanced they appear. These are execution variables that ultimately determine whether the strategy can be implemented as underwritten or whether governance constraints begin to reshape the outcome. Structuring to Preserve Speed These dynamics point to a few practical governance principles. First, align control with the operating model. If the thesis depends on speed, decision rights should enable timely action at the management level. Second, reserve approvals for truly fundamental matters, not routine operating decisions that occur frequently. Third, define thresholds that reflect how the business will actually run, including pre-approvals for expected activities like add-ons and incremental leverage. Fourth, make approval processes workable in real time, not just balanced on paper. This is where experienced counsel matters. In this context, “sophisticated governance” means more than drafting protections; it involves translating the investment thesis into a decision-rights framework that will function under time pressure. That includes calibrating reserved matters, setting practical thresholds, designing board composition and quorum rules, and stress-testing deadlock outcomes against realistic scenarios. The goal is to preserve investor protections while ensuring the company can execute without repeated escalation. Closing Thought Strategic partners can add value, particularly where they address real capability gaps or strengthen the financing narrative. In many cases, they improve the quality of the deal and increase the probability of closing. But they also introduce a second layer of governance that must align with how the business will operate after closing. If that alignment is not addressed before close, it tends to be addressed afterward, when decisions need to be made quickly and flexibility is limited. That is where execution risk increases and the original thesis begins to drift. Not because the strategy was flawed, but because the structure does not support it. If you are navigating this dynamic in a live deal, it is worth addressing decision rights early and in practical terms — before they become constraints in the first 100 days.

April 23, 2026

Business

The Great Ownership Transfer: Why Execution Breaks Search Fund & ETA Deals

Most commentary on the “Great Ownership Transfer” or the "Silver Tsunami" focuses on sellers. It is right there in the name. Aging owners. Lack of succession planning. Uncertainty around exit. That framing is incomplete. This is not just a supply story; it is a buyer capacity problem. Particularly for search fund entrepreneurs, independent sponsors, and others pursuing entrepreneurship through acquisition McKinsey estimates that ~6 million SMBs will face ownership transitions by 2035, representing up to $5 trillion in enterprise value. Yet roughly 92% of exits are likely to occur through closure, not sale. McKinsey Report: The Great Ownership Transfer. If you are acquiring businesses in the $500K–$25M range, your primary competition is often not another buyer. It is the business quietly shutting down. This Is Not a Deal Flow Problem - It Is a Buyer Execution Problem in Search Funds and ETA There is no shortage of businesses to buy in the lower middle market. The challenge for search funds, independent sponsors, and ETA buyers is execution. It is likely that for some of these businesses, the rational step is closure, but there will remain a significant number of profitable businesses in search of a buyer during this economic event. The problem exists in the shortage of buyers who can: Source effectively Underwrite accurately Finance reliably Transition successfully The gap between going under LOI for a “viable business” and closing is where most deals fail. That gap is also where the opportunities and risks live. The Buyer Capabilities Stack In practice, buyer success in this market comes down to the four capabilities identified above. Sourcing: The Best Deals Are Not in Market Because closure dominates exit paths, many viable businesses never run a formal sell process. They speak with a CPA, a broker, or a peer about selling, and when friction appears, the process stops. Running a sell process is not without its hurdles, which is why the rewards are greater for those who do it. If your sourcing strategy depends solely on brokered deals, you are competing in the most efficient (and crowded) segment of the market. If a buyer wants to improve their odds at wining, they need to: Build referral channels with accountants, attorneys, and advisors Focus on specific industries to accelerate underwriting Embrace cold outreach Engage sellers before a formal process exists The winning edge is not price. It is access to top tier deals that are found through hard work and diligence. Seller Readiness: Most Deals Fail Before Diligence Another recurring issue in lower middle-market transactions is not business quality, but transferability. Common issues that cause buyers to avoid deals include: Incomplete or inconsistent financials Owner-dependent relationships Undocumented processes Unclear working capital needs The better initial question is not: “Is this a good business?” It is: “Can this business be transferred and financed cleanly?” Buyers can use a simple readiness screen when examining prospective companies to purchase by examining for: 24 months of monthly financials and tax returns Customer concentration and contract review Identification of key personnel dependencies Basic operational systems (billing, quoting, payroll) Working capital dynamics post-close Deals that fail this screen rarely improve during diligence. I recently posted about broken LOIs and the reasons why buyers walk away: Broken Executed LOIs By Reason. Over 45% of the reasons for failure can be categorized within the items listed above. Financing: The Constraint Most Buyers Underestimate Financing is not a closing step. It is a very serious pre-LOI workstream. That may seem like an obvious statement, but many failed deals share a common pattern: The buyer underwrites one version of EBITDA, and the lender underwrites another. That gap kills deals. Particularly in SBA-driven transactions common in search funds and small business acquisitions: Equity requirements and guarantees are real constraints Underwriting timelines introduce friction Smaller deals are treated as bespoke, not standardized Disciplined buyers: Underwrite to debt service, not seller-adjusted earnings Normalize add-backs conservatively Identify working capital needs early Seriously consider the structure pre-LOI (seller notes, holdbacks, transition-linked payments) The deal is not real until the capital stack is real. Nothing happens without financing. Post-Close Execution: The First 100 Days Decide the Outcome The most underappreciated risk in these transactions is not closing. It is transition. I believe buyers should familiarize themselves with at least some turnaround management practices during the search process because buyers inherit: Informal systems Relationship-driven revenue Limited reporting infrastructure Outdated systems Without a clear transition plan, value can erode immediately. It is not simply a digital transformation play (digital advertising, industry specific project management Saas, etc.). Effective buyers plan for: Defined transition services from the seller Retention of key employees Structured customer handoffs Weekly cash and operations cadence post-close This is not operational detail. It is downside protection and risk mitigation. It is also some of the hardest work because it cannot be brute forced - it requires soft skills, attention to detail, and time-consuming review of information. What This Means for Investors Backing Buyers For family offices, independent sponsor investors, and capital partners backing search funds and ETA buyers, the underwriting focus needs to shift. Similar to what we discussed above, the question is not: “Is this a good business?” It is: “Can this buyer execute this transition?” Key diligence questions for investors to ask should include: Does the buyer have a repeatable sourcing strategy? Is there a defined readiness filter? Is financing aligned with lender reality? Is a post-close execution plan in place? Most deals in this segment fail due to execution gaps, not thesis failures. The Structural Inefficiency Creates Opportunity The inefficiency in this market is not hidden. It is structural: fragmented deal flow, inconsistent advisor quality, limited financing standardization, and minimal post-close support. These are not isolated issues - they are systemic frictions that sit between a viable business and a closed transaction. Prepared buyers can benefit from this inefficiency because it creates: Less competition in off-market deals Pricing inefficiencies The ability to win through structure and not just valuation But those advantages are only available to buyers who can execute. This is not a market where capital alone wins. It is a market where taking a business from “viable” to “financeable” to “transferable” is necessary and may require a longer pre-LOI/pre-close relationship with the seller. If pre-screening raises concerns around financial quality, customer concentration, or post-close execution, the question is not just whether the deal is attractive. It is whether those risks can be mitigated before committing to an LOI. Most deals don’t fail because the business is bad. They fail because the buyer underestimated what it would take to close and operate it. Spending time with the seller (sometimes weeks or even months) before fully committing can be one of the most effective ways to de-risk a transaction before signing an LOI and set up a smoother, more profitable transition. The Real Takeaway The Great Ownership Transfer is often framed as a wave of supply. The data suggests the real issue is execution. This is especially true for those pursuing entrepreneurship through acquisition, where execution risk concentrates in a single asset. The challenge is not finding viable businesses. It is getting them across the finish line after turning viable businesses into successful buyer transitions, not closures. For buyers, the edge is not just identifying a good business. It is building the capability to move a deal from: possible → financeable → transferable → stable The market does not reward intent. It rewards execution. Buyers who can deliver that consistently will capture disproportionate value.

April 3, 2026

Business

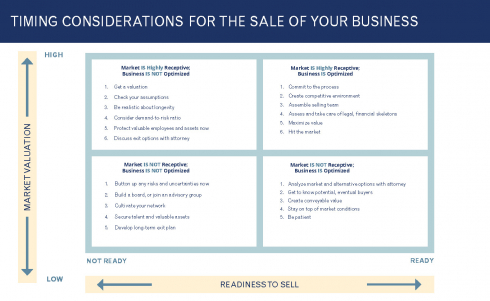

Planning for a Sale: Engineering the Best Possible Outcome