Business

Post-Close Alignment in Lower Middle Market M&A: Where Deal Stress Begins to Fracture

By Mark G. Wendaur, IV

Most sellers and buyers in lower-middle-market M&A, including search funds, entrepreneurship through acquisition (ETA), and independent-sponsor transactions, begin to suffer from deal fatigue and welcome the post-closing phase of a business acquisition or M&A transaction. No more due diligence, no more negotiations, no more redlines. However, in many cases, the post-close phase is fertile ground for additional disputes to emerge.

Most post-closing friction in lower-middle-market M&A deals is not caused by something that was absent from the deal. To the contrary, it is actually related to the negotiated documents governing the relationship between seller and buyer in the post-close transition phase. Consulting agreements, employment agreements, and corporate governance documents in rollover equity transactions seek to govern the relationship, but the relationship is still new in this phase. The parties are experiencing, for the first time, what it is like to work together after the change in dynamics (seller-owner to exited owner; buyer with funding to operator managing debt service and performance expectations).

In this example, the seller rolled equity in the transaction and was now an equity holder in the buyer's platform company. The post-closing issues did not stem from a missing provision, but from ambiguities that existed across multiple documents that were meant to align and work together: seller notes, management agreements, and governance documents were all in play and created more confusion than clarity.

That pattern is more common than most buyers expect, particularly in search fund, entrepreneurship through acquisition (ETA), and independent sponsor deals where post-close roles and governance tend to be more fluid.

The LOI to Close Gap in M&A Transactions

Most of these issues are not created at closing. They are created in the window between LOI and signing.

At LOI, the parties align on high-level economics and general expectations:

- The seller will stay involved

- The business will transition smoothly

- Equity will keep everyone aligned in the case of rolled equity, or amounts due pursuant to the seller note will incentivize cooperation

But those concepts get translated into separate documents depending on the deal:

- Employment agreement

- Consulting agreement

- Operating agreement

- Purchase agreement

Each document answers a different question. Very few processes force those answers to be reconciled into a single operating model.

That is where the gap forms.

By the time you reach closing, the documents are “complete” but not always aligned.

Where Post-Closing Issues Show Up in Business Acquisitions

Employment Terms in Post-Closing Transition

Buyers often assume that key individuals, particularly a selling owner transitioning into an operating role, will continue “as expected.”

The employment agreement is where that expectation either becomes a reality or breaks down. The most common issues include:

- Role definition is too broad or not tied to actual authority

- Termination provisions do not reflect how performance issues will be handled

- Compensation structures do not match the deal model

Example:

A seller stays on post-close in a senior operating role (e.g., general manager) under a two-year agreement while the buyer installs its own CEO or operating partner. The buyer expects to reshape reporting lines and decision-making authority over time. The agreement, however, includes strong severance protections and defines material changes to duties or authority as “good reason.” Six months in, the buyer begins shifting responsibilities to its operating partner. The seller asserts “good reason” and triggers severance or other protections, despite the buyer viewing the changes as part of the planned transition.

Nothing is technically wrong in the document.

It just does not reflect how the buyer intended to transition control of the business.

Consulting Roles and Transition Services Agreements

Consulting arrangements are often treated as secondary or low-risk.

In practice, they can drive real execution outcomes. This is especially true in customer transition and institutional knowledge transfer.

Where this tends to go wrong:

- Scope of services is loosely defined

- Time commitment is not specified

- Compensation is not tied to outputs

Example:

A seller agrees to a 12-month consulting arrangement to support transition. The agreement references “reasonable availability” but does not define hours, deliverables, or response expectations. Post-close, the buyer expects active involvement in customer introductions and onboarding. The seller views the role as limited advisory support that can be provided from a remote location and not on-site.

The result is predictable. The buyer feels unsupported. The seller believes they are complying with the agreement.

Again, nothing is broken in isolation.

The expectations were never aligned.

Rolled Equity and Post-Close Governance

Rolled equity is typically framed as a tool to align the parties in furtherance of a more profitable enterprise. In practice, it can be alignment in concept only, not in execution.

Where this tends to go wrong:

- Different expectations around liquidity timing

- Limited clarity on governance rights

- Misunderstanding of distribution mechanics

Example:

A seller rolls 20% of proceeds into the new structure. The buyer plans to reinvest cash flow into growth and limit near-term distributions. The seller expects periodic cash flow similar to how they operated pre-sale. The operating agreement permits discretion on distributions, but the practical application of that discretion was never aligned.

This is not a legal defect. It is an operating mismatch that surfaces quickly once capital allocation decisions begin.

Why Post-Closing Misalignment Occurs in M&A Deals

During the deal process, these items are negotiated in parallel:

- Purchase agreement

- Employment agreements

- Consulting agreements

- Equity and governance documents

Each document may be internally consistent, but the following question should be asked: Do these documents, taken together, reflect how this business will actually be operated on day one?

More specifically: Do they clearly define what the seller is required to do, what authority they retain or lose, how they are compensated for that role, and what happens if those expectations change or break down?

If the answer to those questions is unclear, the issue is already embedded in the deal.

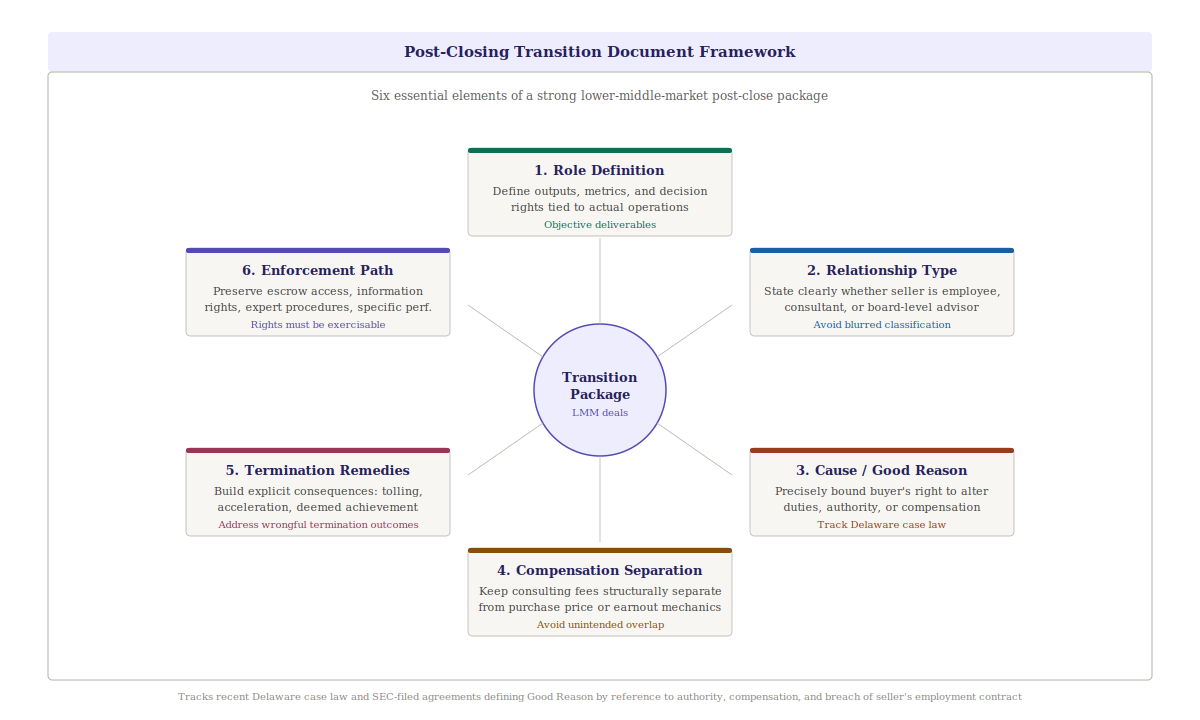

Practical Considerations Pre-Close in Lower Middle Market Transactions

This is almost always easier to address before closing than after.

In practice, a strong lower-middle-market post-close package tends to do six things:

- Define the role with objective deliverables. Move beyond titles. Specify outputs, metrics, and decision rights that tie to how the business will actually be operated.

- Clearly classify the relationship. State whether the seller is an employee, consultant, or board-level advisor. Blurred status tends to create both operational and legal ambiguity.

- Precisely frame “cause” and “good reason.” If the buyer retains flexibility to change duties, reporting lines, compensation, or authority, that flexibility should be clearly bounded. Well-defined “cause” and “good reason” concepts are what translate flexibility into enforceable expectations.

- Separate consulting economics from deal economics. Consulting fees should stand on their own unless the parties intentionally link them to purchase price or earnout mechanics. Unintended overlap often creates disputes about what is being paid for performance versus transition support.

- Build explicit consequences for disruption. If authority is stripped or termination occurs outside the expected framework, the documents should address the outcome. That can include tolling, acceleration, deemed achievement, or extension concepts tied to equity or earnouts.

- Preserve a practical enforcement path. Rights are only useful if they can be exercised. Escrow access, information rights, expert determination procedures, and specific performance provisions tend to make these arrangements function in practice.

Closing Thought on Post-Closing Risk and Deal Execution

These are not technical refinements. They determine whether the post-close relationship functions when conditions change.

Most post-closing issues do not come from a single broken provision. They come from small inconsistencies across multiple documents that were never forced to align into a single operating framework.

If you are under LOI or in diligence, this is typically the window to fix that alignment without disrupting the deal.

After closing, you are no longer interpreting intent; you are operating within the structure you drafted.

If you are working through this in a live deal, step back and ask:

Do these documents, collectively, dictate how decisions get made, how the seller participates, and how economics actually flow?

If not, then the risk is not theoretical. It is already built into the deal.