Business

Investor Equity Placement: Why HoldCo vs. OpCo Matters

By Mark G. Wendaur, IV

When a searcher or independent sponsor brings in outside capital, the conversation often centers on valuation and percentage ownership. But an equally important question is structural:

Should the investor hold equity in the operating company (OpCo) or in the parent holding company (HoldCo)?

This decision carries meaningful legal, economic, governance, and strategic implications. It affects dilution, future capital raises, control dynamics, exit flexibility, and long-term alignment. The analysis also becomes more nuanced depending on the investor’s role and non-monetary contributions.

Consider a common scenario: a sponsor raises $2 million to acquire a $10 million HVAC company, with plans to pursue add-on acquisitions over time. In a roll-up strategy like this, what if one investor brings domain expertise, sourcing capabilities, or operational leadership that materially influences growth? That strategic contribution may justify equity at the HoldCo level, where the investor participates in platform-wide upside and profits.

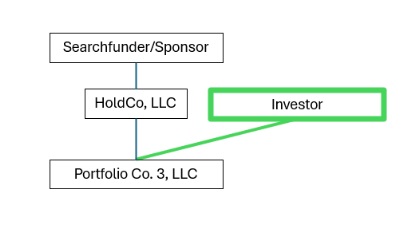

By contrast, a passive investor whose involvement is limited to board oversight may be more appropriately placed at the OpCo level, particularly in a single-asset acquisition. Of course, this assumes the target will operate as a subsidiary rather than being merged into an existing operating entity — which is itself a separate structural decision. An investor in this scenario will usually see investment income flow solely from OpCo (instead of the entire portfolio of companies).

The structure and placement of an investor's equity is rarely mechanical. It should reflect strategy, bargaining power, long-term vision, and investor expectations. The considerations below provide a framework for both searchers/sponsors and investors to consider when evaluating this decision.

The Two Primary Structures

Investor Holds Equity at the Portfolio Company Level (OpCo)

Under this structure, the investor owns equity directly in the acquired operating business. OpCo is typically maintained as a standalone entity or as a clearly defined subsidiary beneath a holding structure.

Key Implications

- The investor’s economics are tied solely to the business of OpCo

- Governance rights are limited to decisions within OpCo

- Exit proceeds flow from the sale or recapitalization of OpCo

- The investor has no direct rights to unrelated subsidiaries or future acquisitions

Common Use Cases

- Single-asset traditional search fund deals

- One-off independent sponsor acquisitions

- Transactions without a broader platform thesis

- Situations where negotiation dynamics support a narrower investment scope

Advantages

- Structural simplicity

- Clear alignment around a single asset

- Cleaner distribution waterfall

- Reduced complexity in governance documents

- Easier return modeling tied to one business

Risks and Considerations

- Limited investor participation in future add-on acquisitions

- Potential need to restructure if platform ambitions later emerge

- Dilution of equity will occur at the operating level if additional capital is raised, although usually unlikely unless part of a larger restructuring

- Misalignment if investors expect exposure to future platform growth

OpCo equity works best when the investment thesis is narrowly defined and neither party anticipates a broader multi-asset strategy. Many first-time searchers/sponsors and their investors will fall into this structure.

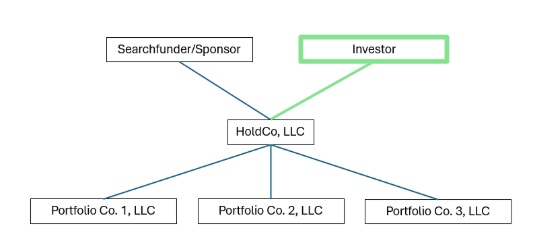

Investor Holds Equity at the Parent Holding Company (HoldCo)

In this structure, a parent entity owns one or more subsidiaries, and the investor holds equity at the parent level.

Key Implications

- The investor participates in the economics of all subsidiaries beneath HoldCo

- Add-on acquisitions can be completed without issuing new OpCo equity

- Governance is centralized at the parent level

- Platform value creation accrues across the entire enterprise

Common Use Cases

- Platform or roll-up strategies

- Independent sponsor models contemplating multiple acquisitions

- Long-term scaling plans involving additional capital raises

Advantages

- Centralized governance and decision-making

- Easier implementation of sponsor promote structures

- Ability to allocate management incentive equity across subsidiaries

- Greater flexibility for future capital formation

Risks and Considerations

- Increased complexity in operating agreements and shareholder documents

- Need for carefully drafted distribution waterfalls

- Cross-subsidiary economic exposure if not properly structured

- Greater sensitivity to dilution stemming from future equity financing

- More robust negotiation of protective provisions and investor rights

HoldCo structures reward forward planning but require thoughtful drafting and clear alignment among stakeholders.

Legal and Governance Considerations

In practice, HoldCo structures centralize power and economics at the parent level, while OpCo structures localize rights and obligations within a single operating entity.

- Where the investor equity sits directly impacts:

- Voting rights and approval thresholds

- Board composition and observer rights

- Protective provisions

- Information and reporting rights

- Drag-along and tag-along mechanics

- Transfer restrictions and liquidity rights

- Put and call rights, if negotiated

If the investor sits at HoldCo, governance documents must anticipate:

- Future equity issuances

- Add-on acquisitions and layered capital structures

- Sponsor promote mechanics

- Reallocation of advisor and/or employee incentive equity pools

- Distribution waterfalls across multiple subsidiaries

- Potential conflicts between legacy investors and new investors

If the investor sits at OpCo, documentation tends to focus more narrowly on:

- Operating distributions

- Exit triggers tied to a single asset

- Seller rollover alignment

These differences materially affect control and economics. They also influence negotiations with senior lenders, particularly where covenants intersect with equity commitments.

Strategic Questions Before Deciding

- Before finalizing entity placement, sponsors and investors should consider:

- Is this a single-asset investment or the foundation of a broader platform?

- Are add-on acquisitions part of the near-term or long-term strategy?

- Will additional investors likely participate in future rounds?

- How centralized should governance be?

- What is the intended exit pathway (strategic sale, recapitalization, long-term hold)?

- How does the structure align with sponsor promote economics and incentive equity?

- Does the investor bring strategic value beyond capital?

Common Structural Mistakes

Frequent errors to keep in mind (and avoid):

- Defaulting to OpCo equity without evaluating long-term platform goals

- Granting HoldCo equity without clearly defining dilution mechanics

- Misaligning promote structures with entity placement

- Overlooking interaction between investor rights and senior debt covenants

- Ignoring tax, estate, or succession planning implications

- Treating entity placement as a documentation detail rather than a strategic decision

These choices are difficult to unwind and can create friction during future capital raises, refinancings, or exits.

Final Perspective

Bringing on an investor is not merely a capital event. It is a structural decision that defines governance, economics, capital formation, and exit flexibility.

Whether you are a search funder acquiring your first business, an independent sponsor building a scalable platform, or a family office co-investing alongside operators, the level at which equity is issued matters.

The best structures anticipate the second deal before the first one closes.

Structure intentionally. Plan forward. Align incentives early.